The U.S. economy is slowing. When the economy slows, hiring slows. When hiring slows, consumer spending typically follows.

Declining consumer spending can further decelerate hiring as business revenues fall, tightening the clamp on consumers and growth. When policymakers at the Federal Reserve observe this pattern, they reach for the only tool they have to reverse it — rate cuts.

Fed Chair Jerome Powell smiled when asked at a Wednesday press conference concluding the central bank’s two-day policy meeting if the ongoing government shutdown — and subsequent data blackout — will soon lead to policy decisions made by anecdotal evidence.

“This is a temporary state of affairs,” said Powell.

For the second consecutive month, the Federal Open Market Committee (FOMC) that sets U.S. monetary policy voted to lower its benchmark rate by a quarter-point, dropping the overnight lending rate for banks to a target range of 3.75% to 4%.

The government shutdown, approaching a full month, has induced a data drought, with most federal offices shuttered. Data relied on to make interest rate decisions typically flows from two main sources: published government statistics and industry contacts.

Though lacking the “very granular understanding” of the economy that federal statistics provide, policymakers relied on private data sources, industry outreach and employment and economic data collected at the state level to reach Wednesday’s decision.

A growing divide

Powell described the rate decision as a “strong vote in favor of this cut,” though he noted “strongly differing views” among policymakers about future policy decisions.

Those differing views arise from policymakers’ unique forecasts of the economy, Powell explained, while mentioning multiple times how “different risk appetites” diversify views on how to proceed.

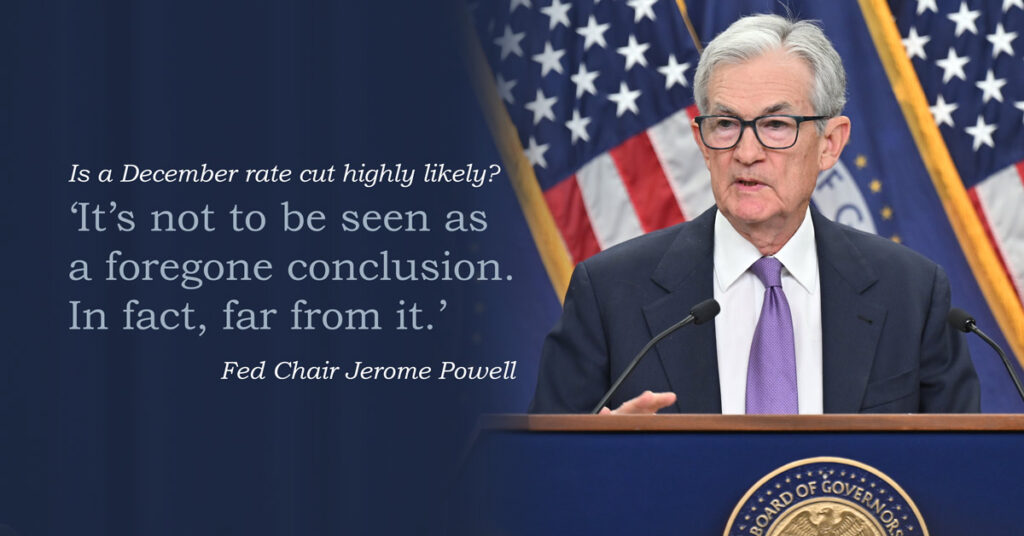

“A further reduction of the policy rate at the December meeting is not a foregone conclusion,” the Fed chair said. “In fact, far from it.”

The Federal Reserve has a dual mandate to maintain stable prices and maximum employment. Though the Fed announces policy on a consensus basis, not all policymakers agreed with Wednesday’s rate cut, as the opacity of underlying economic conditions has worked like a wedge to widen the range of policy views.

Fed Governor Stephen Miran preferred to lower the target range for the federal funds rate by 0.5%. Jeffrey Schmid, president and CEO of the Federal Reserve Bank of Kansas City, preferred no change to the target range.

Despite the annual pace of inflation running at 3% in September, employment risks to the downside remained the driving force behind Wednesday’s decision, as they were last month when the Fed lowered its target rate for the first time in 2025.

Powell described September’s consumer price index report, published during the shutdown due to statutory Social Security deadlines, as “directionally” softer than expected, with inflation not related to tariffs tracking “0.5% or 0.6% closer” to the Fed’s 2% goal than the headline statistic.

The committee also voted Wednesday to end its balance sheet runoff on Dec. 1, a policy move that Powell hinted at in a speech delivered during a recent award luncheon hosted by the National Association of Business Economists.

Runoff from agency mortgage-backed securities (MBS) will be reinvested in U.S. Treasury bonds, Powell said, to better match the longer-duration Treasury holdings currently on the Fed’s balance sheet with the outstanding universe of Treasurys in the market.

A shrinking workforce

Powell underscored in Wednesday’s press conference that the Fed sees stagnant job creation as the result of a dramatic reduction in the supply of new workers due to immigration policy, declining labor force participation and shrinking demand for workers.

Still, initial jobless claims have remained stable, Powell noted, and though the job creation rate and job finding rate are both low, so is the unemployment rate, still around 4.3%.

“We do not see the weakness in the job market accelerating,” Powell concluded.

Recent announcements of major layoffs from the likes of Amazon, UPS, Target and General Motors have signaled corporate America’s renewed appetite for efficiency, and in particular, a thinning of the managerial herd fueled by massive investments in artificial intelligence.

The tensions between growth and employment may be resolving to employment’s detriment but ultimately not AI’s, though Powell hedged on questions about AI’s impact on job creation and whether rate cuts could fuel further AI-driven stock market concentration.

Whether the Fed can stimulate shrinking demand for workers without reigniting inflationary pressures remains to be seen. Powell reiterated that policymakers remain “absolutely committed” to returning inflation to the Fed’s stated target of 2%, even as the central bank prioritizes economic stimulus to prop up the labor market.

“The outlook for employment and inflation has not changed much since our meeting in September,” Powell said, citing a September reading on the personal consumption expenditures (PCE) price index, the Fed’s preferred measure of inflation, of 2.8%. The Fed derived that reading on its own, given that certain inputs typically used to calculate PCE were lacking.

When asked whether the growing policy divisions and accruing dissents make his job presiding over FOMC meetings more difficult, Powell responded, “I wouldn’t say that, no.”

Six weeks now remain before the Fed’s December policy meeting, which will include updated forecasts on the path of future monetary policy in 2026.

“We continue to face two-sided risks,” Powell said. “With today’s decision, we remain well positioned to respond in a timely way to economic developments.”