In its fiscal year 2024 annual report to Congress, the Federal Housing Administration (FHA) shows more than 1.1 million stand-alone partial claims completed since 2020 to help distressed homeowners avoid foreclosure and keep their homes.

An analysis of nearly 1 million of those partial claims in public record data points to the possible shadow side of these claims as a permanent home retention option: a steady draining of home equity that leaves some distressed homeowners at the end of the loss mitigation road with no home and no equity.

Stand-alone partial claims are used to bring delinquent borrowers current on their mortgage through the mechanism of a junior position, zero-interest loan secured by the property. The U.S. Department of Housing and Urban Development (HUD) is the lender, and the loan does not have to be paid off until the first position loan is paid off down the road, typically through a property sale or refinance. Through its partial claim program, FHA allows a total partial claim amount — which can come in the form of one partial claim or multiple partial claims — of up to 30% of the first position loan’s unpaid balance.

While partial claims help distressed homeowners avoid foreclosure by leveraging the ample equity cushion that many homeowners have, they are also letting air out of the equity cushion and even pushing some homeowners underwater. Meanwhile, a group of homeowners are approaching their partial claim capacity limit, putting them in danger of running out of rope when it comes to that foreclosure prevention option.

The analysis looked at more than 958,000 partial claims completed since 2020 based on loan type, loan amount and lender name in public record data. Those claims were on 710,000 properties, a ratio of 1.34 claims per property.

The good news is most properties with claims still have ample equity — at least on paper. Even with the partial claims factored in, properties with partial claims have an average estimated equity of more than $140,000, assuming the property is in good condition and not in need of major renovation.

The bad news? That average equity of $140,000 is more than $27,000 lower than the average equity of $167,000 without factoring in the partial claims. Homeowners in effect are exchanging their equity for no house payment for a period of several months, or longer.

For homeowners with a short-term hardship that prevents them from making their mortgage payment for a relatively brief period of time, this exchange of equity for housing payments will likely leave them better off in the long run. They keep the home despite a temporary life disruption, after which they continue to make mortgage payments and continue to build equity in the home.

For distressed homeowners facing a more permanent hardship that will keep them from making mortgage payments over the long run, the partial claim simply delays the inevitable loss of the home even while draining equity that the homeowner could have walked away with.

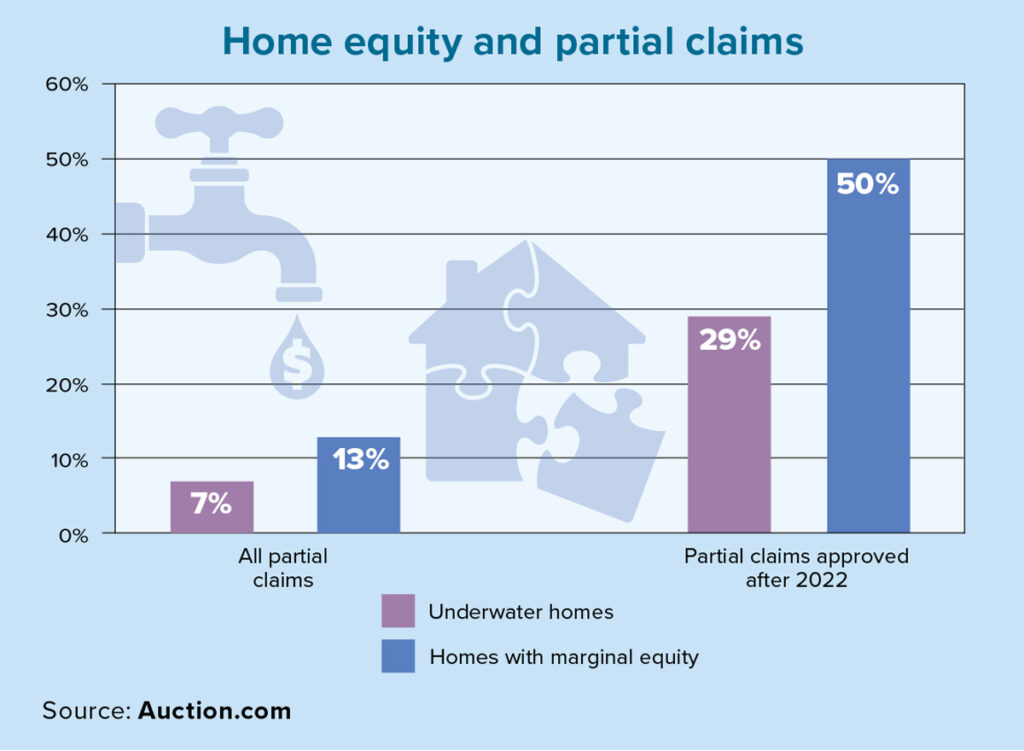

The public record analysis found that 7% of properties with at least one partial claim were underwater, meaning the property was worth less than the total debt secured by the property. Another 6% had less than 10% equity.

The underwater and marginal equity numbers were significantly higher for more recent loans originated in 2022 or later — not surprising given those represent homes purchased near the peak of the market with slowing home price appreciation since purchase. Among those recent loans with partial claims, 29% were underwater and 50% had marginal equity (10% or less).

Additionally, more than 1 in 5 properties with a partial claim (23%) had used up at least 80% of total partial claim capacity — the 30% of the unpaid loan balance — while 13% had completely exhausted total partial capacity.

Loss mitigation data from HUD also shows evidence that more distressed homeowners are running out of options to avoid foreclosure. The number of “loss mitigation option failures” for FHA-insured loans averaged more than 29,000 a month in 2024, up 53% from about 19,000 a month in 2023, according to the HUD Neighborhood Watch portal.

While partial claims have provided a creative loss mitigation option to help hundreds of thousands of distressed homeowners avoid foreclosure at the expense of equity in the short term, the partial claim well is drying up for an increasing number of distressed homeowners who face long-term hardship.