Health care real estate is a diverse sector. Unlike other real estate areas which primarily focus on one type of business, health care is more nuanced and contains several subsectors.

For example, health care real estate includes a wide variety of senior housing options, such as assisted living, independent living, memory care and community care retirements centers, to name a few. Beyond those general categories, health care properties also include skilled nursing facilities, medical office buildings, life science (e.g., research and development and biomanufacturing) spaces and, of course, hospitals.

Each segment of this real estate sector has different risk characteristics, including whether reimbursement rates are from public or private pay mechanisms. For example, “stroke of pen risk,” the risk that a change in the rules governing an industry could impair a company’s financial performance, is an important consideration in the health care field. It is an especially important consideration when dealing with government organizations such Medicare or Medicaid and for those investing in skilled nursing facilities and hospitals.

With 2024 being a presidential election year, Democrats and Republicans are already publicly positioning their stances on such issues and the rhetoric is likely to ramp up as the general election approaches on Nov. 5. Senior housing and medical office buildings, however, are typically mostly private pay, so in that sense, their underlying credit risk tends to be more insulated.

When it comes to health care, there are shared drivers across property types, including one of the most powerful, aging demographics. According to the 2021 American Community Survey, nearly 17% of the U.S. population fell into the 65-plus age cohort which has been increasing over time. In 1970, for example, the 65-plus age cohort accounted for 9.8% of the total population. Moreover, the U.S. population ages 65 and over grew nearly five times faster than the total population over the 100 years from 1920 to 2020.

Thus, the population demographics over the next decade are indicative of robust demand. Given there will always be a need for providing care for the elderly, including rehabilitative services and developing life-saving drugs, the sector is often considered to be defensive.

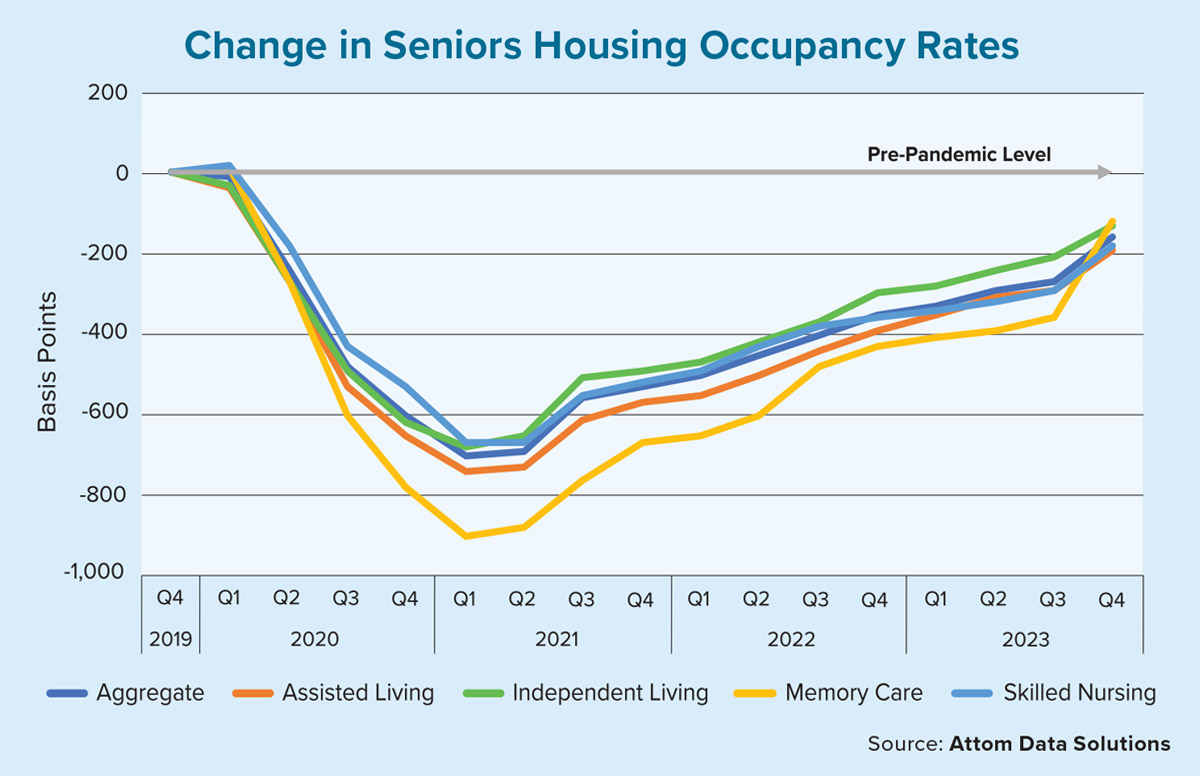

The U.S. Census Bureau’s projections have spurred developers — especially ones specializing in seniors housing — to prepare for the forthcoming “silver tsunami.” In anticipation of these aging baby boomer trends, the supply of senior housing increased at a compound annual growth rate of approximately 2% from 2014 to 2019. Supply growth slowed at the onset of the COVID-19 pandemic, however, falling to 1% from 2019 to 2023. Consequently, moderating levels of new supply coupled with steadfast demand have led to the 11th consecutive quarter of rising seniors housing occupancy gains, according to data from Moody’s’ Analytics.

Although not quite back to pre-pandemic occupancy levels, the current run rate implies the U.S. is likely to achieve parity in the second half of 2024. The aggregate occupancy rate for senior housing was 88.4% as of fourth-quarter 2023, which was 160 basis points lower than the pre-pandemic level of 90% — using the fourth quarter of 2019 as a proxy.

For all the talk of favorable long-term demand drivers, it’s also important to note that there are still several headwinds facing the sector. Aside from political and regulatory risks, rising labor costs and a shortage of qualified nurses are two factors that have been pressuring operators’ already thin margins. Additionally, despite the negative implications associated with higher financing costs, this has led to a moderation in new supply, which perhaps perversely, has helped contribute to the occupancy gains.

Just how much agreement (or lack thereof) that comes out of Washington to reshape the health care industry remains to be seen. While the adage “if you build it, they will come” can be interpreted as a sign of the over exuberance from developers, as 2024 progresses, it will likely become more apparent that those long-awaited efforts are starting to bear fruit.