Likely wearing a nondescript blue suit, on Wednesday afternoon Federal Reserve Chairman Jerome Powell will shuffle behind a nondescript podium in a nondescript press room at the Federal Reserve headquarters in Washington, D.C., to announce one of the most consequential monetary policy decisions of his central bank tenure.

Powell is not expected to defy financial markets operating under the assumption of an imminent 25-basis-point cut to the overnight borrowing rate for banks. Nor is Powell expected to heed the demands of President Donald Trump, who for months has waged a divisive rate-cut pressure campaign, at one point calling for the benchmark federal funds rate to be set somewhere between 0.25% and 1.75% instead of its current range of 4.25% to 4.5%.

In fact, Powell and his fellow central bankers are not expected to do anything surprising. As of Tuesday afternoon, just 4% of futures traders are predicting a jumbo rate cut of 50 basis points, according to the CME FedWatch tool. The other 96% think a quarter-point rate cut is in store, with the odds of the Fed holding rates steady sitting at zero percent.

Recession ahead?

Mark Zandi tells Scotsman Guide that if he were on the Federal Open Market Committee — the Fed’s 12-member voting body that sets interest rate policy — he would vote to lower the fed funds rate by 25 basis points, eyeing an imperative to focus on economic growth.

“I think it is critical for the Fed to avoid going into a recession,” says the chief economist of Moody’s Analytics, a global ratings agency. “Obviously because that would be difficult on American people, but also because it might be existential with regard to the Fed [and] their independence moving forward, so they need to make absolutely sure we don’t go into a recession.”

Zandi believes economic recession risks are currently “very high” and supported by warning signals flashing from stalled job creation. Inflation expectations, on the other hand, remain “well tethered at least in the bond market,” he says, supported by the expectation that tariff-driven prices hikes will not prove persistent.

Still, he thinks the goal for the Fed should be to ensure that recent upticks in inflation do not grow entrenched over the next six to 12 months.

Doug Duncan, former senior vice president and chief economist at Fannie Mae, does not believe the U.S. is on the cusp of recession and attaches the prospects for renewed job creation to businesses’ need for certainty more than a small rate cut.

“In addition to increases in the prices of some goods,” Duncan says, “to this point tariffs have contributed increased risk premiums to interest rates due to the uncertainty of the ending point of tariffs.”

The near certainty of at least a 0.25% rate cut this week is based on the belief that a deteriorating labor market is of more pressing concern than inflation, which rose 2.9% annually in August based on consumer price index data.

Labor vs. inflation mandate

The Federal Reserve has a twofold mandate of promoting both stable consumer prices and maximum employment. The former goal entails 2% inflation rate over the long run. The latter isn’t strictly defined, though a 4% unemployment rate is often used as a general benchmark.

When the jobs market slackens, a Fed rate cut can have a stimulating effect by lowering borrowing costs and encouraging companies to hire. But if inflation is running hotter than the Fed’s stated goal, cutting interest rates can compound that problem.

Though the pace of inflation is higher than ideal, a series of dour jobs reports over the summer revealed alarming hiring trends.

In August, the Bureau of Labor Statistics (BLS) drastically revised May and June’s payroll growth figures by 258,000 jobs — the largest downward revision since 1968. Additionally, the unemployment rate ticked up to 4.3% in August, a Labor Department report published Sept. 3 showed the number of unemployed workers exceeding job openings for the first time since 2021, and fresh BLS data has indicated job creation was weaker in 2024 than previously reported.

“The rising initial unemployment claims and the high level of continuous claims, along with the back-to-back [downbeat] nonfarm payroll reports, make a solid case that the job market is indeed weakening, which needs all the help it can get from the Fed,” says Preetam Purohit, head of hedging and analytics at Embrace Home Loans.

Purohit tells Scotsman Guide that the surprise factor will be how federal courts rule on the legality of the Trump administration’s global tariffs, “and how the entire flow of goods settles down once all the deals are settled.”

Tariff-induced price hikes and inflationary pressures from a shrinking labor supply have complicated the Fed’s decision-making as labor market jitters overshadow long-run inflation.

“I don’t expect significant additions of employment until the tariff picture becomes clear or immigration pressures ease,” Duncan says. “The Fed’s tools have a greater ability to address inflation than employment. Some people may say that’s hard-hearted, but I think it’s the opposite. It respects maintaining people’s purchasing power.”

Will a Fed rate cut matter for mortgage rates?

Mortgage rates take their cue from Treasury bond yields. The 30-year fixed-rate mortgage, for example, is benchmarked to the 10-year Treasury note and is calculated by adding a spread to the 10-year yield.

Duncan sees the uncertainty over the ending point of the effective tariff rate contributing to increased risk premiums on interest rates. He anticipates mortgage rates closer to 5.5% through 2026 if risk premiums related to the U.S.’s willingness to pay its debt and inflationary effects of debt expansion disappear — or closer to 6.5% should those pesky pressures on yield spreads persist.

Lisa Sturtevant, chief economist of Bright MLS, the second-largest multiple listing service in the U.S., thinks mortgage rates have already baked in some of the expected Fed rate cut.

“We should not expect rates to drop much further,” Sturtevant tells Scotsman Guide. “And, in fact, there is a possibility that mortgage rates could actually increase after the Fed cut.”

This is because “investors may infer that the Fed has taken their eye off inflation and worry that inflation expectations are still high,” she explains. “As a result, they will demand a higher yield on investments, including investments in U.S. Treasurys, pushing those Treasury yields higher.”

Selma Hepp, chief economist at real estate market analytics firm Cotality, says the Fed may take a more cautious approach to additional rate cuts in upcoming meetings as labor market concerns come into focus, bearing in mind rising inflationary pressures.

“I think there is slow and painful improvement in the housing market and I think that will continue because there is more inventory,” Hepp says, “because affordability is making strides. It’s not going to be super exciting in 2026, but I do see it as being better than 2025.”

Data uncertainty

Following President Trump’s firing of BLS Commissioner Erika McEntarfer in the wake of a poor July jobs report and the hefty revisions to May and June’s employment estimates, uncertainty surrounding the Federal Reserve’s statistical inputs has added another wrinkle to the central bank’s interest-rate calculus.

Erica Groshen, former commissioner of the BLS from 2013 to 2017, tells Scotsman Guide that survey response rates have fallen by more than half since 2015. Funding and staffing cuts by the Trump administration only compound that problem, she cautions.

“Lousy data would give you lousy decisions, so the Fed could overreact or underreact to current economic conditions and therefore raise interest rates or lower interest rates in ways that weren’t good for the economy,” she explains. “And then there’s the international influence, which is people become less certain about the U.S. economy and their investments in the U.S. economy.”

Sustained uncertainty has a way of trickling through the economy, impacting consumers’ and businesses’ spending outlook and overall faith in the market. Perhaps nowhere is that sentiment more impactful than bond markets, where a spike in interest rates could occur independent of the Fed’s rate decision.

Bond prices and yields have an inverse relationship. When bond prices rise due to increased demand, yields fall. Conversely, a bond sell-off causes prices to drop, leading to a spike in yields.

How will bond markets react to a Fed rate cut?

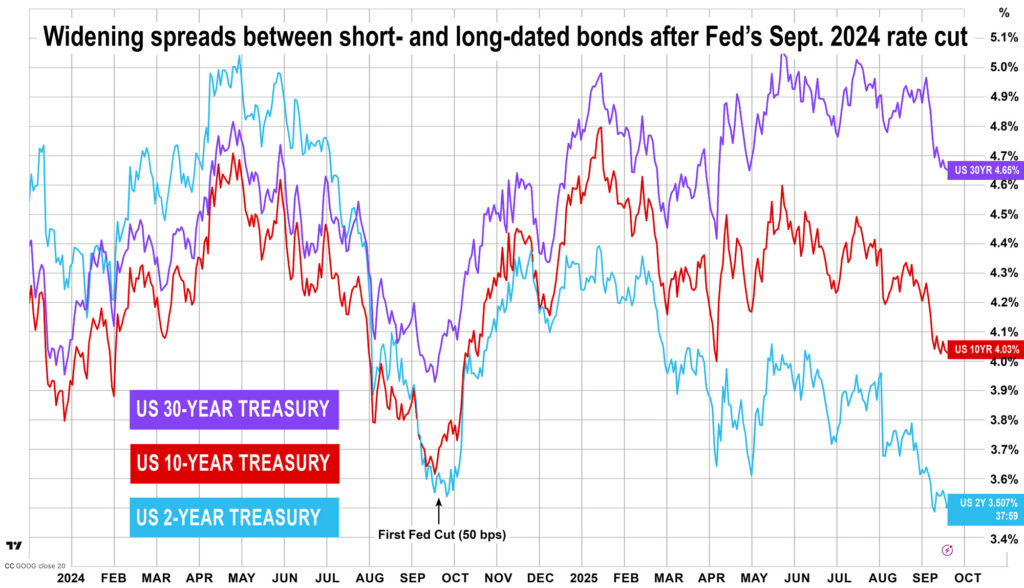

As the U.S. continues to expand its deficit while failing to trim spending and raise taxes, the frequency at which the U.S. rolls its debt over has risen as demand for long-term Treasurys falls and demand for short-term Treasurys increases. Meanwhile, the neutral rate on the 10-year Treasury bond is projected to gradually reset 20 basis points higher over the next decade.

“I don’t know that investors have bought into the idea that these big deficits will start driving up interest rates, at least to the degree that we’re anticipating,” says Zandi, the Moody’s chief economist. This is due to most investors’ shorter-term focus, he says.

Zandi thinks market participants should be prepared for the possibility that the ballooning federal deficit could result in a widespread bond market sell-off.

“If we are for higher long-term rates going forward, it will expose imbalances in the financial system that might exist that are difficult to know or to see or to anticipate without stresses,” says Zandi, calling it “prudent for investors, lawmakers and businesspeople to consider the probability that there will be some kind of crisis in the bond market where interest rates spike at some point in the not-too-distant future.”

“I think that’s a real threat that needs to be considered,” he says. “I don’t know when, I don’t know what the catalyst will be, I’m not sure how it will manifest, but all the preconditions for that kind of scenario are coming into place.”

The so-called “sell America” trade that intensified in April — whereby investors trimmed exposure to Treasury bonds en masse following Trump’s tariff policy announcement — illustrated the erosion of U.S. debt as a safe-haven asset.

Any mass exit from U.S. Treasurys, or even a shift away from Treasurys as a preferred reserve asset, carries massive implications on its value and yields — implications that are highly uncertain.

“If you just look at the 30-year to 10-year spread, it’s gotten quite a bit wider as investors have become more worried about the sustainability of the U.S. debt load in the long run,” says Preston Caldwell, chief U.S. economist at the ratings agency Morningstar.

He thinks investors are still struggling to understand how potential impacts of the U.S. debt load could evolve given a range of economic and political factors.

“Overall, I don’t think that there is an imminent crisis,” says Caldwell. “If you look at the trajectory of U.S. government debt, it is set for a steady but not a rapid increase in coming decades and it isn’t likely to reach a level which would make a crisis inevitable.” This affords time for fiscal corrections, though Caldwell concedes, “perhaps the market will have to panic a little bit in the short run in order to force policymakers into action.”

The contrarian take: Raise rates

When the U.S. issued trillions of dollars in Treasurys to keep the economy afloat during the COVID-19 pandemic, fear flushed global investors out of other asset classes in a sprint for safety that created “peak bonds,” says economist and technical analyst Francis Hunt, founder of the online trading community The Market Sniper.

Hunt thinks the 40-year bull market for bonds ended because of U.S. fiscal and monetary policies implemented during the pandemic — a reversal posing far more severe consequences than he thinks investors, markets and consumers realize.

“Everyone is expecting financial repression out of bonds to hopelessly underperform for multiple decades,” says Hunt, explaining his outlook to Scotsman Guide.

“You should be raising rates,” he continues. “We need double-digit rates right now to get over the debt-based collapse properly.”

Hunt warns that failure to overcome that debt-based collapse could result in lower valuations for financially leveraged assets, like housing or commercial real estate.

Another argument for a rate hike

The consequences of a synchronized debt crisis unfolding across Western economies like the U.S., United Kingdom and France would entail higher borrowing costs, tighter credit underwriting and larger required deposits for collateralized loans like mortgages.

America’s middle class has been shrinking since the 1970s, but that trend could accelerate in a debt market collapse, as the cost-of-living crisis that defined 2024’s presidential election would likely deepen, amplified by government cuts to entitlement programs.

Consumer spending accounts for roughly 70% of U.S. gross domestic product but increasingly depends on spending by high-income households to fuel demand, which functions as a signal and symptom of rising wealth disparities in the U.S.

Christopher Thornberg, economist and founding partner of Beacon Economics, a market research and consulting firm, believes job market concerns have been overstated, as have recession concerns.

“If anything, they should be cranking the rate up to try and cool things off,” Thornberg says, citing stock market outperformance and elevated price-to-earnings ratios for U.S. equities.

The U.S. has been importing roughly $1 trillion annually over the past two years in “hot money,” Thornberg observes, with investors “chasing yields because yields in the U.S. are better than anyplace else.” He links that trend to the lack of larger increases in interest rates in the wake of expansions in deficit spending.

Cutting short-term rates tends to put downward pressure on the dollar because investors tend to chase higher rates and run from lower rates. “Hot money” will not disappear, but arrive more slowly, Thornberg assesses.

Though he expects a 25-basis-point rate cut on Wednesday, Thornberg worries it may only intensify the broader trend toward higher yields on longer-dated debt, which would add upward pressure to mortgage rates.

“Cutting the federal funds rate seems more likely to be steepening the yield curve than reducing rates across the board,” Thornberg cautions.