What manual asset verification

is actually costing you

A Scotsman Guide featured sponsor

What manual asset

verification is

actually costing you

A Scotsman Guide featured sponsor

Asset verification doesn’t make the headlines, but it might be quietly eating your margin. A borrower submits their application, and then the real work begins: tracking down bank statements, chasing incomplete documents, and reworking errors that shouldn’t have made it into the file in the first place.

Published March 26, 2026

Asset verification doesn’t make the headlines, but it might be quietly eating your margin. A borrower submits their application, and then the real work begins: tracking down bank statements, chasing incomplete documents, and reworking errors that shouldn’t have made it into the file in the first place.

Published March 26, 2026

Manual asset verification rarely shows up as a single line item—it hides in processor hours, loan officer callbacks, and underwriter time spent assembling files that should have arrived complete. That cycle is expensive whether or not it ever gets measured, and it takes a toll on borrowers too. Being asked repeatedly for the same documents during one of the most stressful financial transactions of their lives erodes trust—and leads to borrower drop-off.

Go digital, cut the chase

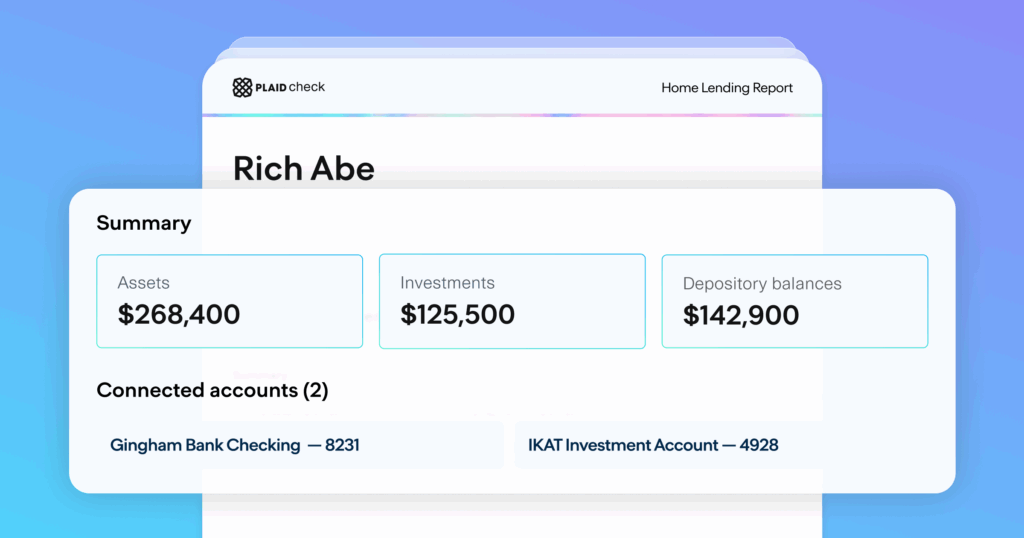

Digital asset verification changes the core mechanic. Instead of asking borrowers to retrieve and submit documents, lenders give them the option to securely connect their financial accounts directly within the application flow. With their permission, lenders access account data from financial institutions in real time—including balances, transaction history, and account ownership.

For underwriters, that means receiving a complete, current file rather than assembling one from PDFs. For loan officers, it means fewer callbacks. For processors, fewer document review cycles. Verification that used to take days can happen in minutes.

There’s a data quality advantage too. Information sourced directly from financial institutions is more reliable than manually uploaded documents, which can be incomplete or vulnerable to fraud. Underwriters work with more confidence when the data comes straight from the source.

“Plaid isn’t just keeping up with the market, they’re leading it. That means we can stay ahead too, delivering the latest and greatest experience for both borrowers and our team.“

Wayne Steagall

Technology Director,

Advisors Mortgage Group

What digital asset verification looks like in practice

Advisors Mortgage Group, one of New Jersey’s most active purchase lenders and the top partner for the NJ Housing and Mortgage Finance Agency, offers a useful window into what this shift can mean at scale.

The company had been running a manual verification process that asked borrowers to download, print, and upload their financial documents—a friction-heavy step that created persistent operational strain. After piloting Plaid’s Home Lending Report from Plaid Check, Advisors moved from a costly, document-heavy process to a streamlined verification workflow—cutting manual touchpoints and reducing reliance on legacy solutions. Borrower uptake followed quickly: Advisors saw a 67% increase in borrowers choosing digital verification over their previous method, reflecting not just convenience, but confidence in the process.

The operational gains translated directly to the bottom line. By reducing reliance on manual workflows and legacy verification solutions, Advisors has projected up to $250,000 in annual savings. Wayne Steagall, Technology Director at Advisors Mortgage Group, credited one capability in particular: “The refresh capability has been a game changer. Instead of calling borrowers back multiple times, the data is automatically updated. That saves our team countless hours and gives borrowers a smoother, more secure experience.”

Plaid’s Home Lending Report also addresses a risk dimension that manual processes can’t. It delivers structured asset data approved by the GSEs for submission—qualifying lenders for rep and warranty relief on verified loans. For underwriters, that’s not just cleaner data, it’s data that comes with a layer of built-in protection.

Scale without adding headcount

One of the more significant benefits for growth-oriented lenders is what digital verification does to capacity. When each loan requires fewer manual touchpoints, your existing team can handle more volume without a proportional increase in cost—a meaningful lever when hiring is expensive and margins are tight.

Advisors found they could close loans faster and compete against larger lenders without adding staff. That advantage shows up in cost structure, but also in speed to close.

Calculate how much going digital can save you

The savings potential varies by lender depending on loan volume, staffing, and how heavily your operation relies on manual document collection. But the math is worth running.

Plaid’s Digital Mortgage ROI Calculator lets you model the potential impact for your specific operation—factoring in loan volume, current verification costs, and expected efficiency gains. If you’re not sure what digital asset verification could mean for your cost per loan, it’s a quick exercise that tends to produce a number worth paying attention to.

"Adoption happened naturally. Nearly all of our loan officers opted in on their own, because it just made sense—Plaid makes life easier for them, our underwriters, and our borrowers."

Wayne Steagall

Technology Director, Advisors Mortgage Group

Plaid powers the tools millions of people use to lead healthier financial lives. Our mission is to build a more inclusive, competitive, and resilient financial system by simplifying payments, transforming lending, and advancing the fight against fraud. More than 7,000 companies, including leading fintechs, crypto firms, Fortune 500 enterprises, and many of the largest banks, rely on Plaid to give people greater choice and control over their money. Headquartered in San Francisco, Plaid connects to over 12,000 financial institutions across the US, Canada, the UK and Europe.