Housing affordability remained worse than historical norms in most county-level U.S. markets in the first quarter.

However, more homes were affordable than during the previous quarter and year-ago levels, says a report released Thursday by real estate market analytics firm Attom.

To afford a nationally median-priced home and keep major monthly expenses below a recommended 28% of wages threshold, assuming a 20% downpayment, a buyer in the first quarter of 2026 would have had to earn $84,230 annually, down from $86,611 a year ago.

Supporting gradually improving affordability is wage growth that outpaced home-price growth in about two-thirds of U.S. counties over the past year. It marks a reversal of a persistent trend since roughly 2011 when home prices gains have outpaced median wage growth.

Attom data shows the nationwide median home price was $351,000 in the first quarter of 2025, which rose about 2.56% to $360,000 in the first quarter. Since the first quarter of 2024, the national median home price has risen 8% while average weekly wages have increased by 6.4%, says Attom, a much smaller gap than in recent years.

Multiple years of double-digit home-price appreciation during the COVID-19 pandemic exacerbated the growth gap between earnings and home prices, entrenching what Attom’s report shows is historically poor housing affordability across most local U.S. markets.

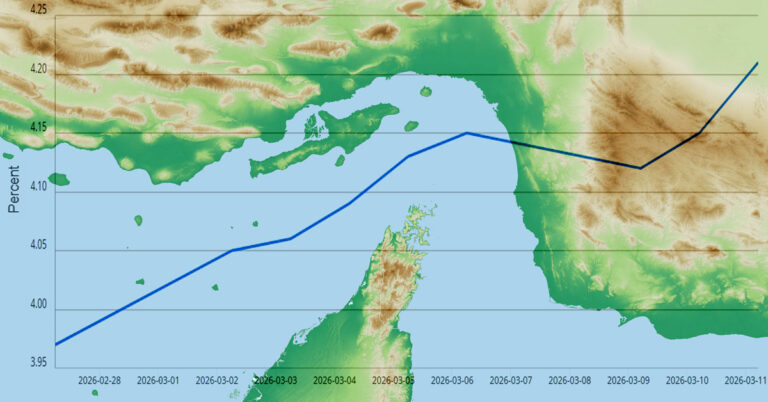

Average mortgage rates for 30-year fixed-rate home loans declined steadily from around 7% at the start of 2025 to the high-5% range in February, also contributing to improved affordability in the first quarter. Those gains have been pared since the start of the Iran war on Feb. 28 fueled a global energy shock that has sent mortgage rates back above 6.4%.

“Mortgage rates dropped throughout last year, which offset some of that growing affordability gap, but shifts in the broader economic environment can still influence rates and home purchasing power,” said Rob Barber, CEO of Attom, in commentary accompanying the report.

The most populous counties where wages rose faster than home prices over the past year were Los Angeles County, Calif.; Cook County, Ill., which includes Chicago; Harris County, Texas, which includes Houston; Maricopa County, Ariz., which includes Phoenix; and San Diego County, Calif.

The geographic distribution of broader affordability gains has been slight, however.

Among the 580 counties Attom analyzed, major monthly expenses for median-priced single-family homes and condos exceeded historic norms in 560 counties in the first quarter, or around 97%. Median-priced homes were less affordable than historical norms in 98% of counties analyzed in the fourth quarter and more than 97% of counties a year ago.

Attom assesses that the typical monthly cost of mortgage payments, homeowners insurance, mortgage insurance and property taxes on a median-priced home nationwide would have consumed 30.3% of a typical worker’s wages in the first quarter, down slightly from 30.6% in the prior quarter and 31.6% in the first quarter of 2025.

In nearly 25% of counties analyzed, first-quarter home purchase expenses exceeded 43% of the typical county resident’s wages, a threshold considered seriously unaffordable, down from nearly 30% of counties that were seriously unaffordable in the previous quarter.

Of the 25 counties where typical monthly home expenses required the greatest share of residents’ wages, California claimed 14, New York claimed four, New Jersey had three and two were in Hawaii.