Emergency loss mitigation programs during and after the COVID-19 pandemic helped hundreds of thousands of homeowners avoid foreclosure, but some of those programs drained home equity.

A growing number of homeowners who utilized those programs are now falling back into default and facing foreclosure with little or no equity left, making foreclosure harder to avoid, with a short sale often the only option.

First noted in our “Beyond the Bid” column in March 2024, data showed equity loss was the trade-off for foreclosure delays — even amid rising home prices.

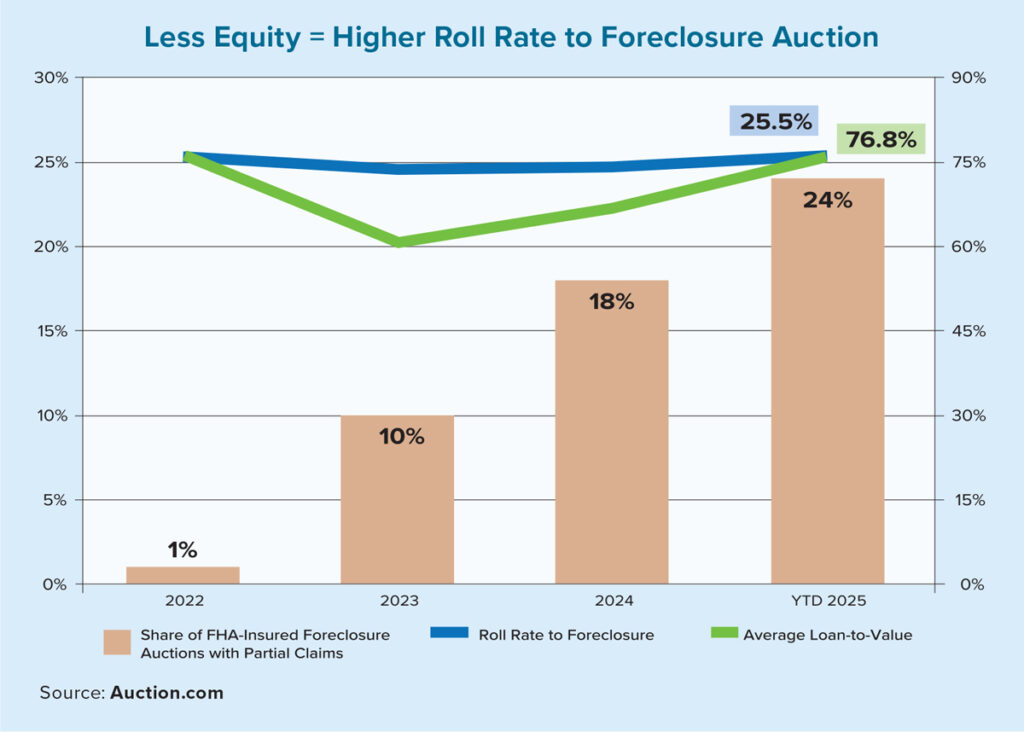

The unintended consequences of prolonged foreclosure delay tactics became apparent by April 2025. By then, many Federal Housing Administration (FHA) partial-claim properties were underwater or had marginal equity. The share of underwater and marginal equity homes with partial claims was exponentially higher among those with mortgages originated in 2022 or later.

More distressed homeowners who used delay options are again facing foreclosure, but with less equity, new data shows. The share of FHA-insured loans at auction with partial claims jumped from less than 2% in 2022 to nearly 24% during the first 10 months of 2025, according to Auction.com data. Additionally, partial claims rose from 1.07 per property in 2022 to 1.39 from January to October 2025, meaning more borrowers took multiple claims before foreclosure.

More than 9,400 properties were brought to auction on FHA-insured loans through the first 10 months of 2025, up 15% from the same period in 2024 and up 74% from the recent low seen during a foreclosure moratorium in 2021.

Homeowners now have less equity due to mitigation programs and falling prices. One-third of markets have experienced a home price correction since 2022, according to ICE data.

The average loan-to-value (LTV) ratio of properties brought to foreclosure auction increased on a year-over-year basis for five consecutive months through November 2025, hitting a 17-month high in September. The higher the LTV ratio, the lower the equity.

The declining equity trend is more pronounced for the FHA-insured book, with average LTV ratios on properties brought to auction increasing annually in 17 of the last 18 months, hitting a 44-month high in November. Average LTVs through October 2025 were at a four-year high for FHA-insured loans brought to foreclosure auction.

Homeowners with less equity are less likely to avoid foreclosure. The share of scheduled foreclosure auctions that were completed in October hit a 34-month high that month for all loan types.

The good news is that more mortgage servicers are adopting programs and procedures that help distressed homeowners avoid foreclosure by selling prior to the foreclosure auction — even if that sale ends up being a short sale.

One Florida homeowner facing foreclosure sold her property through an option for private sellers from Auction.com after proactively contacting her mortgage servicer. They were able to successfully navigate a complex short sale and transition into newly built senior housing that better fit her lifestyle and budget.

“There’s only 38 units, and I managed to snag one,” she said. “I’m moving in tomorrow, so I’m very excited.”