The U.S. office-sector vacancy rate jumped by 30 basis points in second- quarter 2022 to finish at 18.4%, according to Moody’s Analytics data. While this was less than the pandemic-era peak (18.5% in Q2 2021), it marked a significant departure from the generally positive performance that offices had realized over the previous nine months.

Particularly concerning is that the vacancy rate increase is much more related to softening demand rather than robust supply. In fact, net absorption was negative for the first time in a year. The net figure of 8.4 million square feet vacated amounts to the second-largest quarter-over-quarter reduction in occupied stock since the COVID-19 crisis began. Is this a sign that the long-expected deterioration of office performance is upon us, or is this just another pothole on the sector’s bumpy road to recovery?

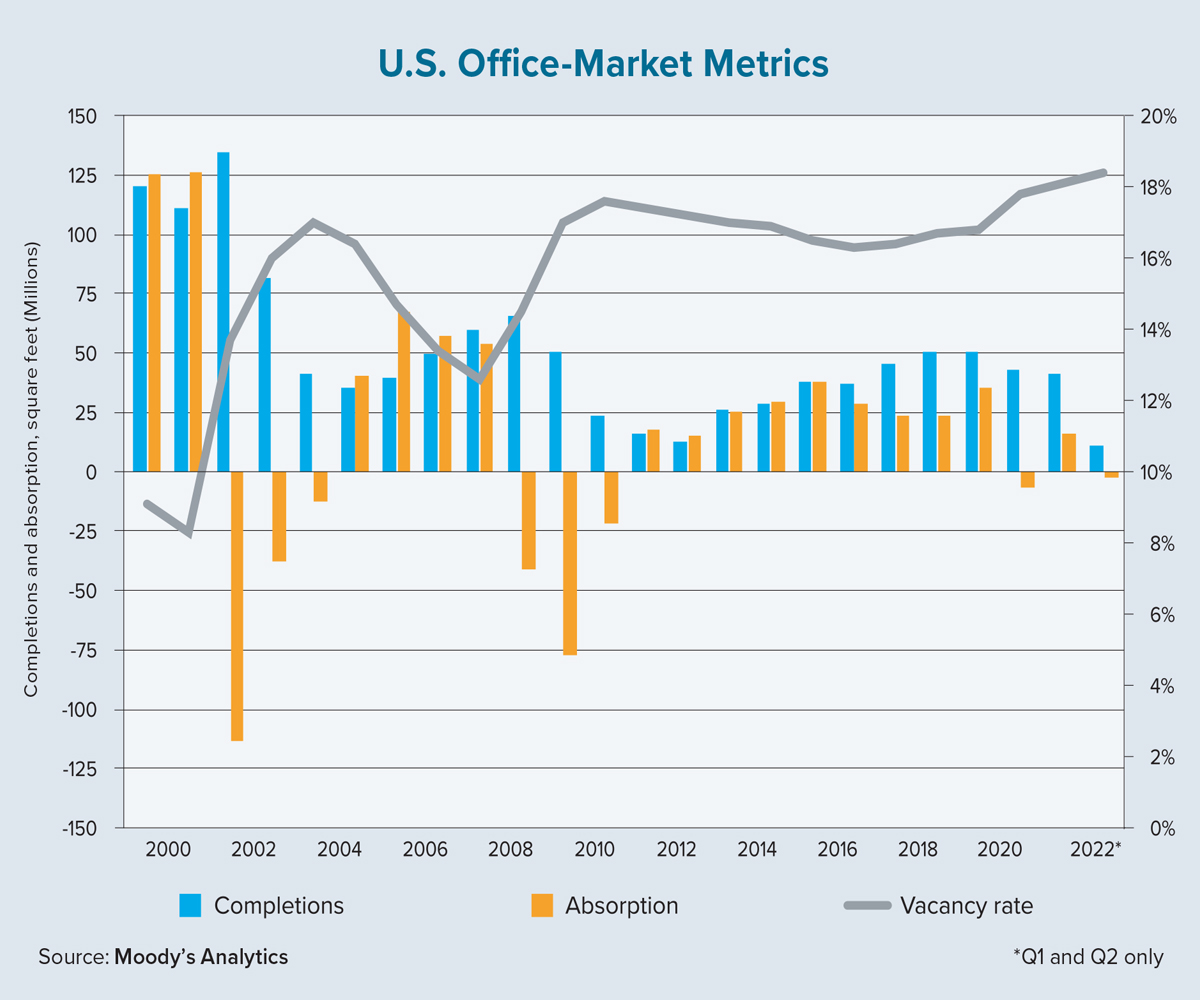

To answer this question, it’s helpful to look closer at how recent trends hold up against previous periods of economic difficulty. The chart on this page notes the substantial decline in net absorption during the bursting of the dot-com bubble in the early 2000s as well as the more recent financial crisis.

From 2001 through 2003, net absorption in the office sector dropped by a total of 163 million square feet. From 2008 through 2010, the aggregate loss reached 140 million square feet. Comparing these figures to the 7.3 million square feet of positive net absorption since early 2020 shows how the most recent downturn has been by far the most benign in comparison.

During earlier downturns, the economic headwinds were financial in nature, with many companies collapsing or permanently laying off a large share of their workforce. The current lull has been health related and free from significant declines in profitability or labor. In fact, over the past few years, firms have remained quite profitable, and even if they weren’t using their office space due to remote-work policies, their real estate costs were minimal enough in relation to their overall level of revenues.

That said, the relative lag in performance deterioration during the previous two recessions also is noteworthy. In these instances, office-sector performance declines continued well past the economic trough. Lease length, traditionally averaging in the six- to 10-year range (with some lasting 20-plus years) is much to blame. If a company is solvent, it will likely wait until its lease expires to condense space.

This is particularly important in the current climate as companies are still early into their respective remote-work experiments. This means that any lag in office-sector performance may not occur for years. Adding to this, economic headwinds are building. A recent uptick in COVID-19 infection rates, along with a slowing of the economy due to the Federal Reserve’s quest to curtail inflation, further complicates the situation. This is a unique moment for the office sector as the shock of remote work is colliding with the shock of a slowing economy.

The level of stress this combination ultimately produces for the office sector will be heavily based on two main factors. One is the productivity and innovation gains or losses tied to remote-work policies. The other is the depth of the predicted economic slowdown. Results are thus far mixed on the productivity front, but some of the more rigorous studies lean negative.

May 2022 data from the U.S. Bureau of Labor Statistics shows there is still room for softness in the labor market, given the roughly 2-to-1 ratio of job openings to the number of unemployed people. We believe this combination of factors is enough to push the office vacancy rate near 19% by the end of 2023, but it won’t cause an exodus on the level of the dot-com bust or Great Recession era.

If the U.S. happens to enter a deeper or longer-term period of economic malaise, firms will likely shed labor and office space as in past downturns, but the magnitude of these actions may be different. Even if remote work proves to be less productive, the option to use it may allow office demand to become more elastic to economic shocks.

Tenants may demand shorter or more flexible leases going forward, allowing for slight cost reductions through the elimination of space without the need to dramatically cut their labor force. This could prove valuable given the future expectations of a tight labor market and persistent skill shortages. ●