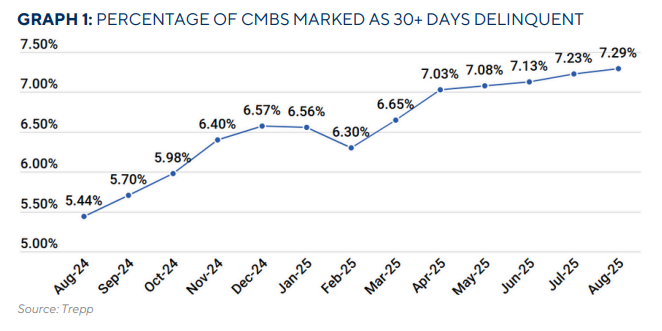

Driven by continued deterioration in the office and multifamily sectors, the delinquency rate for commercial mortgage-backed securities (CMBS) increased for the sixth consecutive month in August, rising six basis points to an all-time high of 7.29%. The overall U.S. CMBS delinquency rate was 5.44% one year ago.

The latest figures from Trepp, a property analytics firm, reflect a commercial real estate market still struggling to find financial footing following major disruptions wrought by the COVID-19 pandemic, from plummeting demand for office space to the growth of e-commerce.

In August, the overall delinquent balance grew nearly 1% to $44.1 billion from $43.3 billion the month prior, while the outstanding balance rose to $604.6 billion from $598.9 billion. Delinquency rates in the multifamily and office sectors worsened, though retail improved.

Rising 71 basis points from July, multifamily delinquencies reached a nine-year high of 6.86% last month, more than double the 3.3% multifamily delinquency rate in August 2024.

Meanwhile, office delinquencies rose 62 basis points to 11.66% in August, with newly delinquent office loans reaching $2.5 billion against $1.3 billion of loan cures. The office sector delinquency rate was 7.97% last August.

On the positive side, the retail delinquency rate dropped 48 basis points to 6.42%, its lowest level in the past year. More than $700 million in cured retail loans offset $300 million in newly delinquent loans in August, according to Trepp.

But the percentage of seriously delinquent loans across property types rose to 6.88% in August, up five basis points from July.