The U.S. hotel sector concluded 2025 in a state of stagnation. The slowdown emerging halfway through the year gave way to flat performance in the final months, signaling weak momentum heading into 2026.

This marked the definitive end of the post-pandemic “revenge travel” boom, a shift driven not by a single shock, but persistent economic uncertainty and dwindling savings for households. Consumer caution has simultaneously weakened occupancy rates and pricing power.

As the tailwinds of pent-up demand and excess savings faded, travelers became more price sensitive in 2025. Late-year data confirmed this stagnation was broad-based. Standout performers during the pandemic’s leisure travel surge, such as Tucson, Ariz., began to experience sharp declines in performance.

While some gateway markets like San Francisco saw temporary, conference-driven boosts from events like the Dreamforce conference put on by Salesforce, these were event-driven outliers and not signs of a fundamental recovery in routine business travel. This underlying weakness stems from companies remaining cautious with travel and entertainment budgets amid persistent economic uncertainty. Many firms are prioritizing essential, client-facing trips, substituting internal meetings with virtual formats as a cost-control measure.

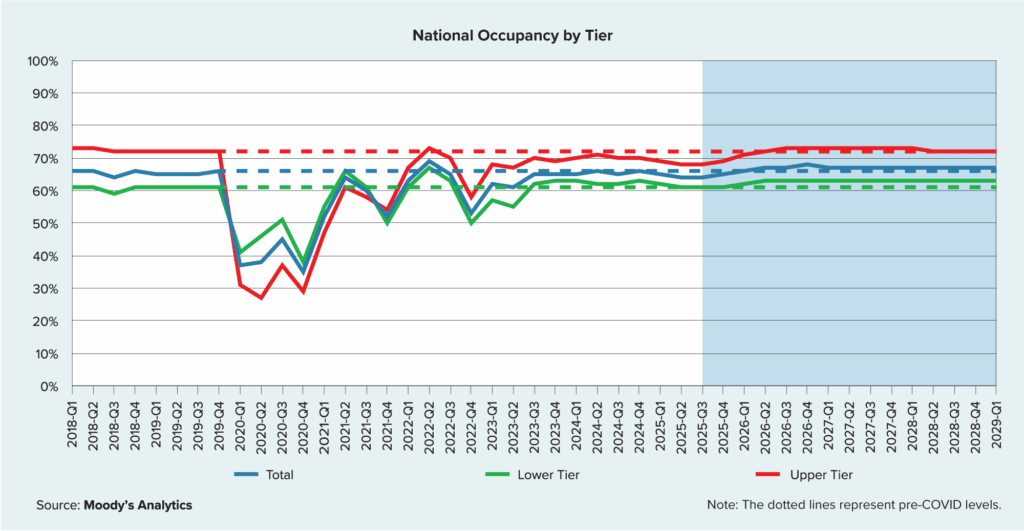

The market’s deceleration is evident in key performance metrics from the second half of the year. Following a third quarter where national occupancy declined for a second consecutive time to 63.8%, causing revenue per available room (RevPAR) to fall 3.2% year over year, fourth-quarter indicators confirmed that occupancies had stabilized at these lower levels.

Stability came at the expense of pricing power as operators’ ability to raise rates weakened significantly. The slowdown was felt across all segments. Upper-tier RevPAR (including luxury, upper-upscale and upscale chain scales) declined by 1.9%. Lower-tier (including upper-midscale, midscale and economy chain scales) slipped by a larger 3.2%, indicating that budget-conscious travelers were not just trading down, but in many cases, pulling back on travel altogether.

The chart below highlights the broad-based decline in occupancy, with both upper- and lower-tier segments decreasing through the first three quarters of 2025:

The slowdown in hotel demand occurs even as the Transportation Security Administration travel throughput data remains robust, often exceeding pre-pandemic levels. The divergence highlights the growing market share of short-term rentals, with platforms like Airbnb and Vrbo capturing a significant portion of leisure travel demand, particularly for families and groups.

An imbalance in international travel has further pressured the sector — Americans increasingly travel abroad while inbound international visitation has not yet fully recovered from the pandemic, driving a net deficit for domestic hotels.

While the lack of year-end momentum in 2025 suggests a weak start to 2026, the outlook for the full year ahead suggests a rebound. Moody’s baseline forecast anticipates RevPAR growth approaching 4.9%, a rate that would outpace inflation. This recovery hinges on stabilization in the leisure and corporate travel segments. Leisure travel is expected to normalize from its post-pandemic surge, as the initial wave of high-spending travel gives way to more typical, budget-conscious behavior.

A full recovery in business and group travel appears unlikely, however, as companies remain cautious with spending amid economic uncertainty. Consequently, the sector’s recovery will be uneven. The upper tier’s revival will remain constrained by weak corporate demand, while the lower tier’s performance should hold steady as it retains its share of price-sensitive travelers, providing a more stable, albeit lower-growth foundation.