In 2020, the COVID-19 pandemic upended not only the U.S. hospitality sector but the entire global economy. The ensuing lockdowns resulted in the steepest drawdown in hotel revenue per available room (RevPAR) since 2000 when Moody’s Analytics began collecting data on hotels. RevPAR, which is a hotel’s average daily room rate (ADR) multiplied by its occupancy rate, is a popular way to measure the economic health of hotels.

The U.S. hospitality industry has more than recouped its losses from the early 2020s recession, but new challenges have emerged that are once again testing the sector’s resilience. Battle-hardened hotel operators who survived the impacts of the historic COVID pandemic are now dealing with a slowing economy and changes to U.S. trade and immigration policies that are posing fresh challenges.

While the average room rate across the nation was effectively unchanged in the first quarter of 2025, a decline in occupancy led to the biggest drop in RevPAR since the first half of 2023. That said, the sequential decline in RevPAR was modest and primarily affected lower-tier hotels, which tend to be low-cost, mid-level to upper-mid-level facilities.

Demand for lower-tier hotels tends to be mostly driven by cost-conscious domestic travelers. Given the lingering effects of inflation and near record-low consumer confidence, tighter discretionary budgets have likely weighed on performance. In contrast, RevPAR for upper-tier hotels — comprising upscale, upper-upscale and luxury properties — remained effectively flat quarter over quarter.

“The U.S. hospitality industry has more than recouped its losses from the early 2020s recession, but new challenges have emerged that are once again testing the sector’s resilience.”

This segment, which attracts more affluent travelers who generally prioritize brand reputation and premium amenities, has been relatively insulated so far. Additionally, upper-tier hotels are more exposed to fluctuations in business travel and international tourism.

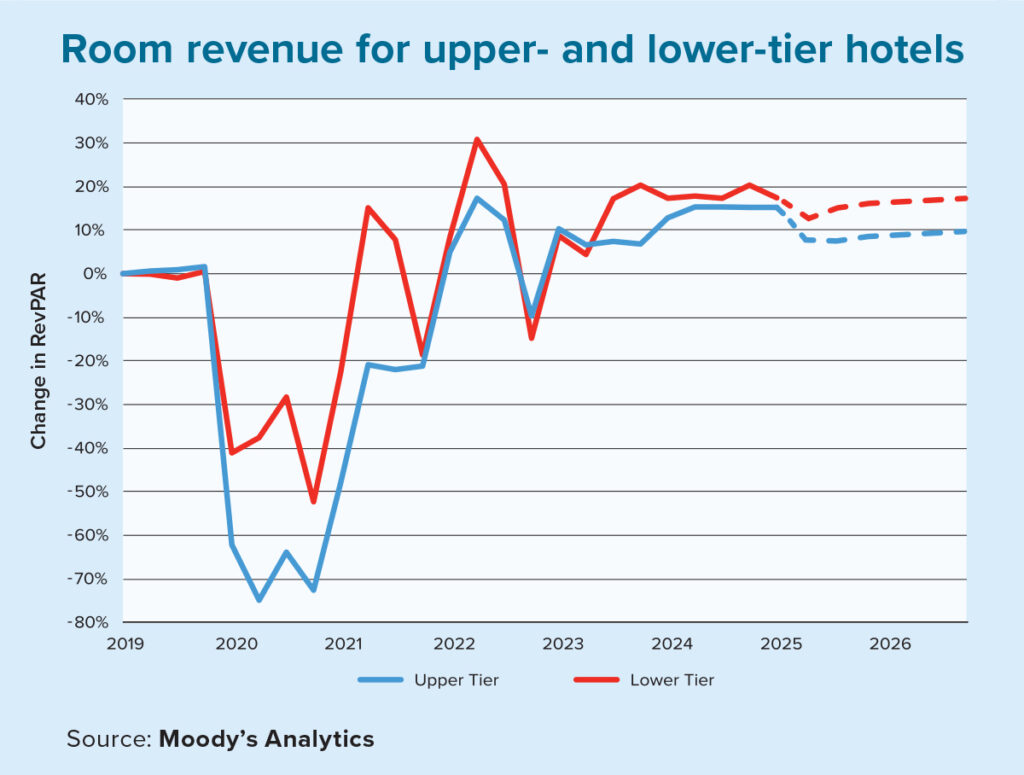

In the first quarter of 2025, upper-tier hotels outperformed their lower-tier counterparts. Usually, during times of economic distress, lower-tier hotels tend to outperform. This is supported by the chart below, which indexes the cumulative change in RevPAR by tier type to the first quarter of 2019.

The corresponding changes in RevPAR illustrate lower troughs for upper-tier hotels and higher peaks for lower-tier hotels. Moreover, the chart highlights that RevPAR growth for lower-tier hotels is projected to remain modestly above upper-tier hotels through the end of 2026.

It is worth noting that on a dollar basis, RevPAR for upper-tier hotels is more than double that of lower-tier hotels. This does not factor in the comparatively higher expenses for upper-tier properties but rather illustrates the point that lower-tier properties benefit on a percentage basis from a lower starting amount, which can make the percentage increase look more significant.

The key question is whether this is a near-term issue or the beginning of a more serious slowdown as geopolitical uncertainty looms and international tourists reconsider the U.S. as a travel destination. Perhaps a saving grace regarding international tourists is that while they may be hesitant to visit the United States, a weaker dollar (particularly against the euro) could make the U.S. a more attractive destination. In other words, a weaker dollar can serve as a counterweight to falling international travel demand.

Even so, challenges remain, such as a shortage of air traffic controllers, and several tragic airline accidents in recent years have added to travelers’ angst. Whether the first quarter proves to be a blip on the radar or the beginning of a more serious downtrend may come down to the prevailing macroeconomic conditions and rhetoric coming out of Washington.