The office market’s positive momentum we saw in mid-2024 has disappeared. While many firms continue pushing return-to-office mandates, economic uncertainty and C-suite efforts to boost margins through artificial intelligence have halted job growth and slowed real estate expansion plans.

Consequently, the national office vacancy rate, which stabilized in mid to late 2024, is rising again. As of August, the national office vacancy rate rested at a record high of 20.7%. Moreover, market stress is not limited to older and less amenitized properties. It is evident across all class designations.

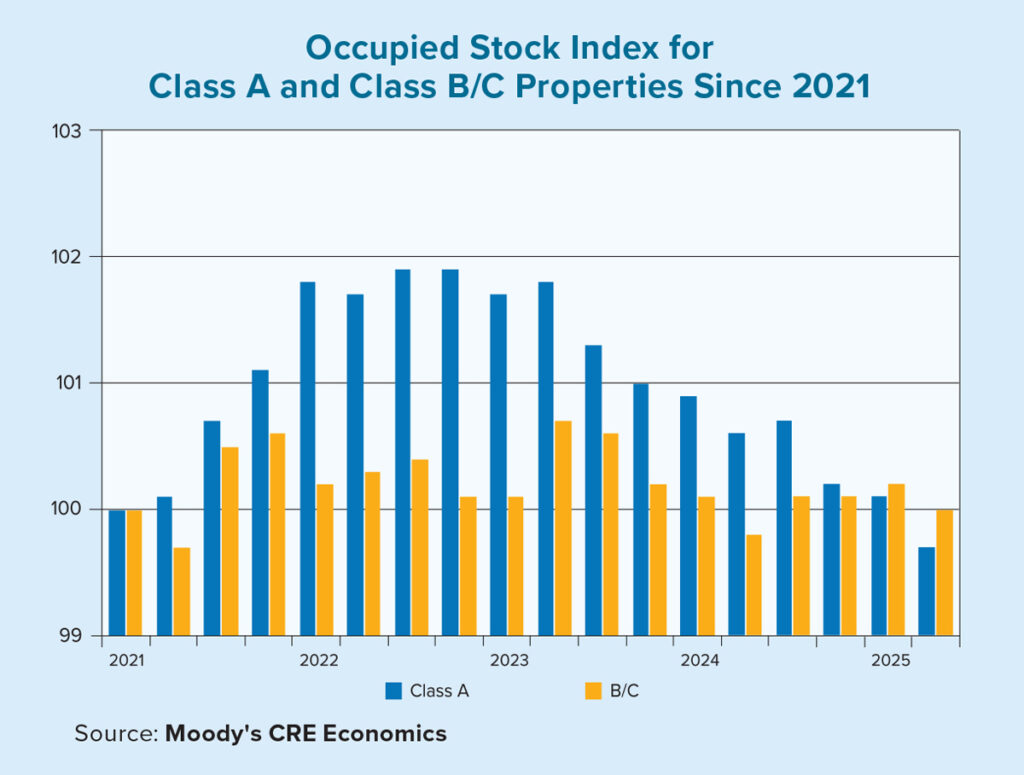

The chart above illustrates the fact by plotting an occupied stock index for Class A and Class B/C properties since 2021. An index above 100 indicates a greater amount of leased space in that period in relation to the first quarter of 2021.

Notice how the “flight-to-quality” momentum realized through early 2023 has fully evaporated. Leased space is now lower for Class A properties than in the early pandemic period. Subtle signs of a potential recovery, emerging in the third quarter of 2024, have vanished, with occupied stock resuming its downward trend.

With the office market contracting, this rightsizing process will lead to entirely vacant office buildings that must be repurposed or razed. Stress on existing office property loans is quickly materializing — the office-backed CMBS delinquency rate surged by about 600 basis points in 2024, marking the fastest annual rise since data collection began in 2000.

“We expect market rightsizing will lead to successful office locations that have consistent levels of foot traffic and vibrancy created by the mixing of land uses.”

For context, the full-year delinquency increase in 2024 exceeded levels observed during the Global Financial Crisis. Alarmingly, however, the first half of 2025 showed the fastest mid-year increase on record, 280 basis points through June, consistent with the accelerated occupancy stress described above.

As always with real estate, nuance is apparent, and success stories emerge for specific office properties in thriving, mixed-use submarkets across nearly all U.S. cities.

The Grand Central submarket of Manhattan offers a good example of a property experiencing ongoing recovery. With continuing public-private initiatives to spur a vibrant mixed-use office-residential-retail corridor, office leasing has accelerated and the vacancy rate has declined nearly 100 basis points in the past year. The positive momentum is not reserved for just newly built or renovated “trophy” properties, as even the pre-2000s built category has a collective vacancy rate well below the national average.

As 2026 approaches, we see national-level office market performance continuing to weaken. New vacancy rate records will be set as 2025 ends, and delinquency and charge-off rates will also rise. But, headline numbers can be deceiving and obscure positive momentum at the submarket and property level.

We expect market rightsizing will lead to successful office locations that have consistent levels of foot traffic and vibrancy created by the mixing of land uses. Thoughtful updates to zoning regulations, along with carefully curated development brought forward by partnerships between municipal governments and deep-pocketed business owners and developers will influence the success of local office markets and specific submarkets that become the new centers of gravity in each respective market.