The retail real estate market is facing significant headwinds, as a combination of bankruptcies, reduced consumer spending and persistent economic uncertainty alters the sector’s trajectory.

Two years of occupancy and rent growth have yielded to stagnation, with potential tenants deferring leasing decisions amid unclear economic and policy environments. Grocery-anchored centers that cater to necessity-driven demand are expected to remain resilient during ongoing economic softness. However, service-oriented tenants are unlikely to fill spaces vacated by struggling goods retailers at the pace observed in recent years.

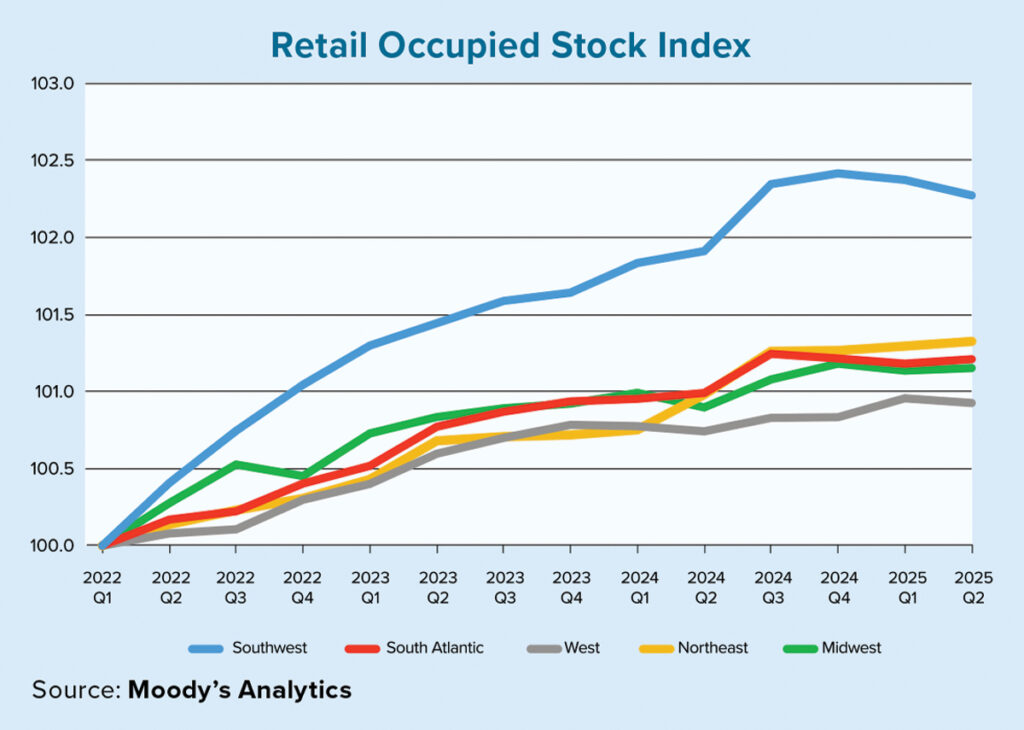

Moody’s Analytics’ real estate update for August reports year-to-date neighborhood and community center rent growth of only 0.4%, with the majority occurring in the first three months of 2025. The data on occupancy growth shows a similar trend, with national occupied stock rising just 1.2 million square feet, or 0.06%.

The Southwest market is leading the slowdown, relinquishing some of the substantial gains made since early 2022. This trend aligns with the performance of other property types across Texas and neighboring states. As affordability benefits fade, firms and households are reconsidering the costs of relocating from other U.S. locations.

This slower migration has weakened absorption rates and caused vacancy rates to rise for office and multifamily properties. Some of these issues will be eased as construction slows, but migration patterns likely won’t return to their pandemic-era peak anytime soon.

“Service-oriented tenants are unlikely to fill spaces vacated by struggling goods retailers at the pace observed in recent years.”

Meanwhile, the Northeast retail landscape continues its slow, steady growth. This growth is supported by increasing return-to-office mandates and stabilized population figures, which boost retailer confidence in expanding into this region.

Against this backdrop, the retail sector’s fortunes are diverging along income lines. Luxury retailers, catering to the top 10% of income earners — whose spending accounts for approximately 50% of total U.S. expenditures and commands the lion’s share of household savings — are expected to weather the storm with relative resilience.

Even if broader economic conditions worsen, this affluent cohort’s spending power should help sustain high-end retail locations and brands.

Conversely, discount retailers specializing in necessities may also fare well, as consumers increasingly trade down to manage household budgets amid uncertainty. This dynamic risks hollowing out the middle of the market — mid-tier retailers that neither attract affluent shoppers nor meet the urgent needs of bargain-focused consumers, squeezed by shifting spending patterns and a polarized retail landscape.

Over the next six months, the outlook for retail spending and retail real estate remains subdued amid economic turbulence. As bankruptcies and reduced consumer confidence ripple through the sector, growth in occupancy and rents is likely to stagnate, particularly outside of necessity-driven segments such as grocery-anchored centers.

Service-oriented tenants, once quick to capitalize on vacated spaces, are now adopting a wait-and-see approach. This further slows the rate of retail churn and contributes to persistent vacancies.

Regional disparities will likely persist, with the Southwest market experiencing waning migration and notable slowdowns, while the Northeast and Midwest markets should continue to see modest, stable gains driven by increased office attendance and population stabilization.

Overall, unless economic clarity improves and consumer sentiment rebounds, retail real estate is poised for continued caution and uneven recovery.