Buying a home continues to be a difficult prospect for the average wage earner across the U.S.

According to Attom’s third-quarter 2025 U.S. Home Affordability Report, median-priced single-family homes and condominiums continued to be less affordable than historical averages in 99% of the counties analyzed by the report. This marked the same numbers seen in the second quarter and continued a trend that has stretched for the past two and a half years.

Affordability concerns have plagued the market during that time span, with home-price gains being matched by mortgage interest rate increases. Recently, however, interest rates have dipped, giving potential homebuyers some margin of relief to counterbalance home prices.

Although the national median home price hit a record high of $375,000 during the third quarter, the average interest rate on a 30-year fixed-rate mortgage dropped from 6.75% in mid-July to 6.26% in mid-September. Unfortunately, lower interest rates could also keep home prices high — and rising.

Since the beginning of 2020, nationwide median home values have increased by 58%, while typical wages have increased by only 28% in the same time frame, a differential critical to the calculation of affordability.

Attom’s affordability metrics are created by calculating the amount of income needed to meet major monthly homeownership expenses (this includes mortgage payments, mortgage and homeowners insurance, and property taxes) for a median-priced single-family home or condo, with an assumption of a 20% downpayment plus a 28% maximum “front-end” debt-to-income ratio. The income necessary to meet those thresholds is then compared to the annualized average weekly wage data from the Bureau of Labor Statistics; anything exceeding 28% of typical wages is considered unaffordable.

Attom analyzed third-quarter data from 580 counties across the U.S., and in 79% of them, homeownership exceeded that 28% threshold, making owning a home unaffordable.

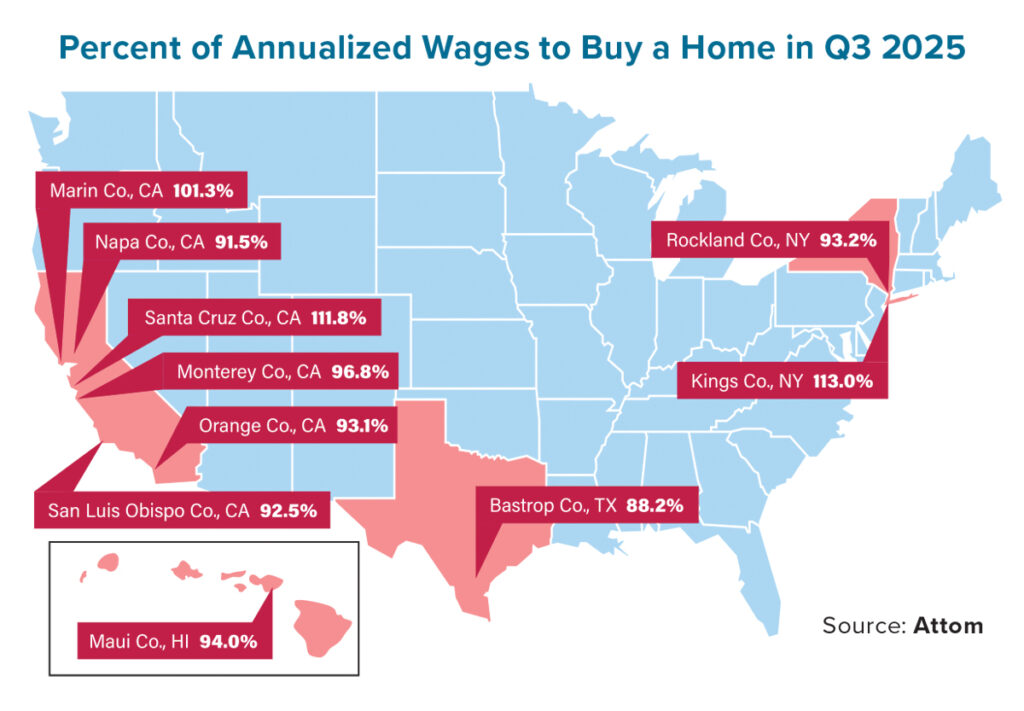

Affordability was an issue in counties with some of the nation’s largest cities, including Los Angeles, Chicago and in New York City’s Brooklyn and Queens boroughs. Homeownership expenses accounted for the largest share of income in the following counties: Kings County, N.Y. (113% of typical annual wages); Santa Cruz County, Calif. (111.8%); Marin County, Calif. (101.3%); Monterey County, Calif. (96.8%); and Maui County, Hawaii (94%).

There were several urban areas that bucked this trend, however. The most populous counties where homeownership expenses accounted for less than 28% of typical wages were: Harris County (Houston area), Texas (23.3% of typical annual wages); Cuyahoga County (Cleveland area), Ohio (23.1%); Allegheny County (Pittsburgh area), Pa. (22.4%); Philadelphia County, Pa. (20.1%); and Wayne County (Detroit area), Mich. (17.1%).

A critical component to affordability is comparing wage growth to home-price increases. The national average wage growth has lagged behind price gains, but that isn’t always the case at local levels. Median home prices grew faster than wages in 49.8% of counties in the report, up from the 34.9% in the second quarter.

The largest counties where home values outpaced wage growth included: Cook County, Ill.; Kings County, N.Y.; Bexar County, Texas; Wayne County, Mich.; and Middlesex County, Mass. On the positive side, however, several counties saw wage growth outpace home-price gains, including: Los Angeles County, Calif.; Harris County, Texas; Maricopa County, Ariz.; San Diego County, Calif.; and Orange County, Calif.

Nationwide, overall homeownership affordability appears better for the average wage earner, while still being unaffordable, however.

The typical monthly homeownership expenses at the national level hit $2,123 during the third quarter; that held steady from the second quarter but was a 6% increase year over year. That total is equivalent to 33.3% of the typical U.S. resident’s wages in the third quarter, up from 33.2% in the second quarter and up from 32.2% in the third quarter of 2024. But in 34.3% of the 580 counties analyzed in the report, homeownership expenses exceeded 43% of typical wages, hitting the “seriously unaffordable” benchmark.

If home prices continue to rise faster than wages can match, owning a home may be more difficult for the average American to realize. With homeownership expenses consuming more and more of wages, these trends will bear watching to see if the decrease in interest rates can help balance out these issues in affordability, or if home prices will start leveling out if too many potential homebuyers are priced out of the market.