The performance of retail real estate is closely linked to the health of the U.S. consumer. How the U.S. consumer fares goes a long way to forecasting how the retail sector will perform.

One sign the consumer is doing well is a low unemployment rate, which is currently near a 50-year low at 3.8% and has remained in the sub-4% range for the past two years. Despite the Federal Reserve’s efforts to tame inflation by raising interest rates, the labor market has not reacted by slowing job creation as in past cycles, with immigration likely a reason behind its unexpected resilience. Sure, the labor market has cooled since 2022, but job openings remain plentiful with approximately 1.4 openings per each available worker. Additionally, job creation has been robust with about 3 million jobs created in 2023.

The first quarter of 2024 showed job creation was off to a strong start, averaging 276,000 new jobs per month. We’ve also seen wage growth outpace inflation since March of 2023 and initial unemployment claims have remained well below pre-pandemic levels. Thus, despite all the calls in 2023 of an imminent recession, the downturn never materialized and the real gross domestic product managed to expand by 2.5%.

Retail trade was the industry making the largest contribution to the expanding GDP in 2023, amounting to 0.58 percentage points of the gain. In a similar vein, retail sales increased by 3.2% for the entirety of 2023 and 4% on a year-over-year basis in March of 2024. The unexpectedly resilient American consumer has not only helped keep the retail sector growing throughout 2023, but also kept the U.S. economy humming along.

That said, there are challenges that lie ahead in 2024. Higher oil prices are a top concern, with crude oil rising to more than $80 per barrel in mid-April. This will ultimately weigh on growth as consumers continue to dip into their savings from pandemic-era aid.

With consumers drawing down their savings, credit card delinquencies have risen. Almost 3.5% of balances were at least 30 days past due at the end of December, according to the Federal Reserve Bank of Philadelphia. That was the highest past-due level since 2012. Additionally, the increasing cost of housing is squeezing discretionary spending levels.

The economic fallout from these crosscurrents has and will continue to be asymmetrical. On the consumer front, there are the haves and have nots, based on household incomes as well as renters versus homeowners status, for example. Lower-income households are disproportionately affected by rising prices, to which we have observed a bifurcation in spending habits between the two groups. While retailers have effectively targeted consumers operating on the lower and higher ends of the income distribution scale, the ‘missing middle’ phenomenon could leave retailers that are failing to adapt to fall farther behind.

One such retailer seeking to adapt in this changing landscape is Macy’s. The company recently announced plans to close 30% of its traditional stores and focus on smaller and smarter layouts. Other retailers, such as Walmart and Target, are utilizing similar strategies to improve sales and minimize overhead.

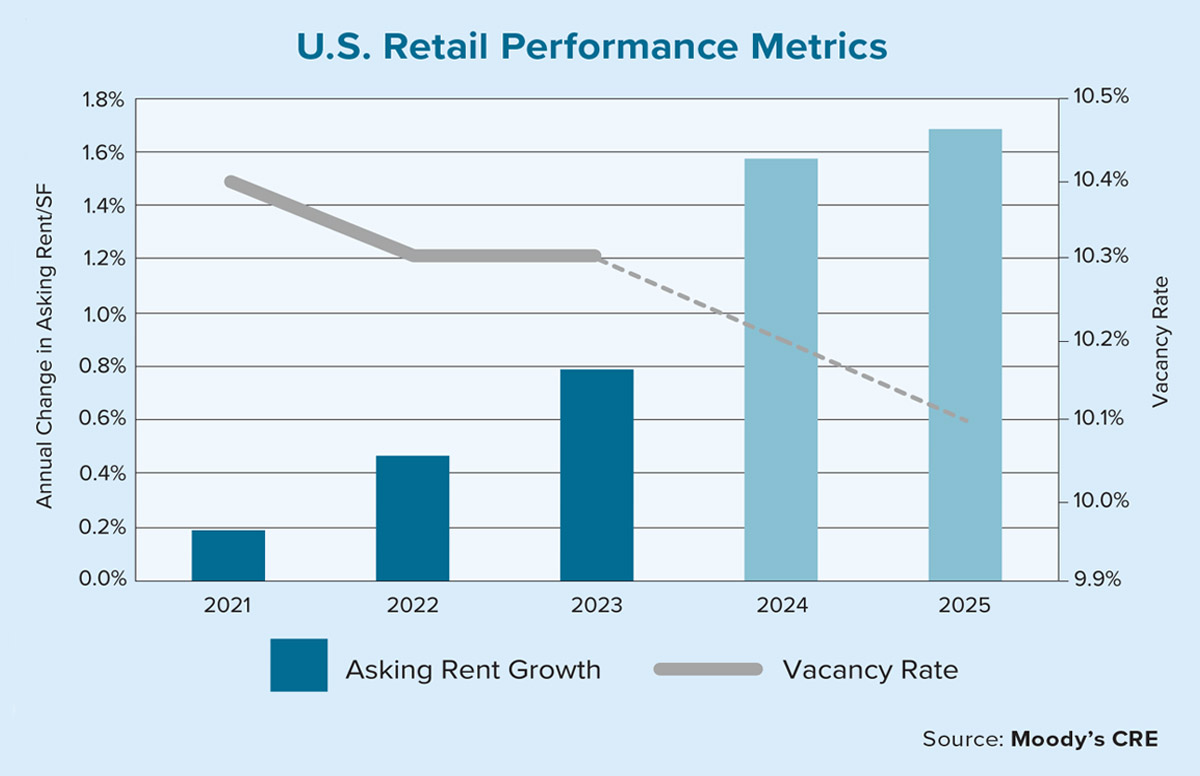

As the accompanying chart illustrates, the retail sector’s year-end vacancy rate has decreased only slightly over the past three years, ending 2023 at 10.3%. While these annual moves measure no more than a dozen basis points, the downward trend is expected to continue during the next two years. As vacancy rates continue to move lower, rents should experience annual increases in the mid-1% range during the same period.

Despite potential danger signs for consumer spending and sluggish retail sales metrics, the sector’s momentum remains to the upside. Retailers continue to adapt, ensuring their relevance and competitiveness as the sector settles into a new equilibrium. ●