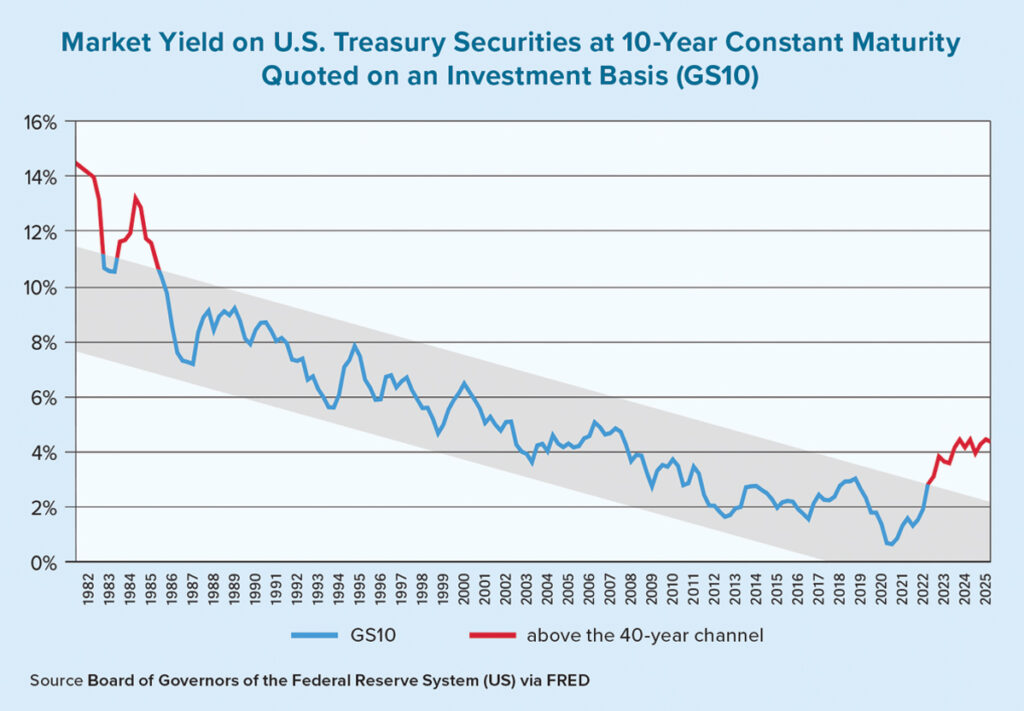

For decades, analysts have charted long-term 10-year Treasury yields through a channel some call the “chart of truth.” It followed the reasoning that financial markets are generally cyclical. Every time bond yields approached the top, they’d council, “Don’t worry, this is where you should buy the long bond. If it’s hitting the upper boundary, it’ll fall back.” These were reliable buying opportunities.

But in 2022, the chart of truth broke.

In technical analysis, the top line of a channel is called resistance. When fluctuations hit it, they generally fall. This time, they advanced above resistance, retreated, then advanced higher again. “Resistance” became “support.”

The clean pattern breakout raised a “bull flag” that signals bond yields could head much higher.

Fiscally reckless deficit spending is one culprit. Even the lowest deficit year post-pandemic exceeds all others, excluding the 2008 financial crisis.

The total U.S. budget is $7 trillion, and we’re adding an average of $241 billion to the deficit every year. Interest payments on the debt exceed $1 trillion in 2025 — around the same amount of money spent on defense.

The rate of debt accumulation pushing total debt higher has reached an inflection point. Once upon a time, total debt was inconsequential, partly because interest rates were so low. During the pandemic, the debt increased by an extreme amount as interest rates increased also. That package is toxic.

If the U.S. doesn’t constrain runaway spending, the debt spiral accelerates. The U.S. is printing money to pay interest on existing debt. We have crossed the threshold at which debt is causing operational disruptions to the government — with no apparent solutions for remediation.

This year, the federal deficit is about $2.1 trillion. The average annual deficit increase pre-pandemic was $135 billion. The post-pandemic average deficit increase is almost double that mark. The rate of debt accumulation has dramatically increased with little political check.

With this supply side problem, who buys the debt? Some foreign entities. U.S. banks and financial institutions are obliged (banks are incentivized to hold U.S. Treasurys as reserve assets). As a result, banks are sitting on larger quantities of overvalued debt. A third entity holding a large volume of federal debt is the Federal Reserve.

At the same time massive fiscal deficits are widening, the Fed’s portfolio of these assets is increasing. It’s called monetizing the debt — printing money and buying those assets and putting them on its balance sheet. The Fed can’t do this indefinitely. It intermittently tries to sell off federal debt.

Quantitative easing (QE) is when the Fed buys assets to support the economy. Quantitative tightening (QT) is the opposite, when it pulls liquidity dollars out of the system. Tightening for too long can create a liquidity crisis. That happened in December of 2019, right before the pandemic. The stock market crashed. The Fed was forced to reverse course and had to inject new money to solve the crisis.

Part of this problem was the pandemic, but most people don’t realize we were in the early stages of recession at that point already. There was a housing market downturn with softening home prices. This was a financial crisis. And then it did a big print during the pandemic. And the Fed bought the debt it printed during the pandemic. That’s where the debt’s all sitting.

Fewer buyers of the debt emerge as overexpenditure funded with overissuance devalues U.S. dollars. Rising long-term bond yields are the inflationary impact of that devaluation, doubling as a tax on U.S. citizens. The interest rate investors demand to purchase U.S. debt rises while a greater portion of tax revenues compelled from U.S. workers funnel into ever-larger interest payments on that debt.

The inflationary effects of currency devaluation show up in higher borrowing costs for consumers, like mortgage rates, as they get benchmarked to higher bond yields. At the same time, hypervaluation of assets accelerates on excess liquidity. Look at pandemic-era home price appreciation of nearly 50% as an example.

Most Americans likely don’t have the patience to understand what’s happening. But without greater understanding, it’s unlikely a proactive political solution will emerge. The experiment is being run. We will see what happens when the Fed prints infinite money to monetize the debt the U.S. Treasury plans to issue over the next decade. Scotsman Guide is buckling up for a rough ride.