Cotality data shows the overall serious mortgage delinquency rate for April 2025 (0.92%) was slightly higher than the previous year, despite a long-term downward trend from a peak of 4.3% in August 2020 to a low of 0.82% in May 2024. Low unemployment rates and a rise in home prices have helped reduce delinquency rates over the past few years

Still, rising inflation, property taxes and insurance premiums could make it harder for homeowners to afford their mortgages, potentially leading to increased delinquencies. In addition, the persistence and severity of natural disasters in some parts of the country can give rise to increased rates of mortgage delinquencies.

Not all loans are built the same. Government-backed loans such as Federal Housing Administration (FHA) and U.S. Department of Veterans Affairs (VA) mortgages are meant to help people with lower incomes or less savings get a foot on the property ladder. They come with lower downpayments and lenient credit score requirements. Such loans have opened the door to ownership for millions of Americans. As of April 2025, the serious delinquency rates for FHA, VA and conventional loans were 3.58%, 2.29% and 0.65%, respectively.

But these government-backed loans come with tighter margins, resulting in less room for unexpected costs. When impacted by natural disasters, unemployment or rise in escrow payments, these borrowers feel it most. Cotality’s data shows serious delinquency rates for FHA loans are five times higher than for conventional mortgages. VA loans are not far behind with three-and-a-half times more serious delinquencies than conventional alternatives.

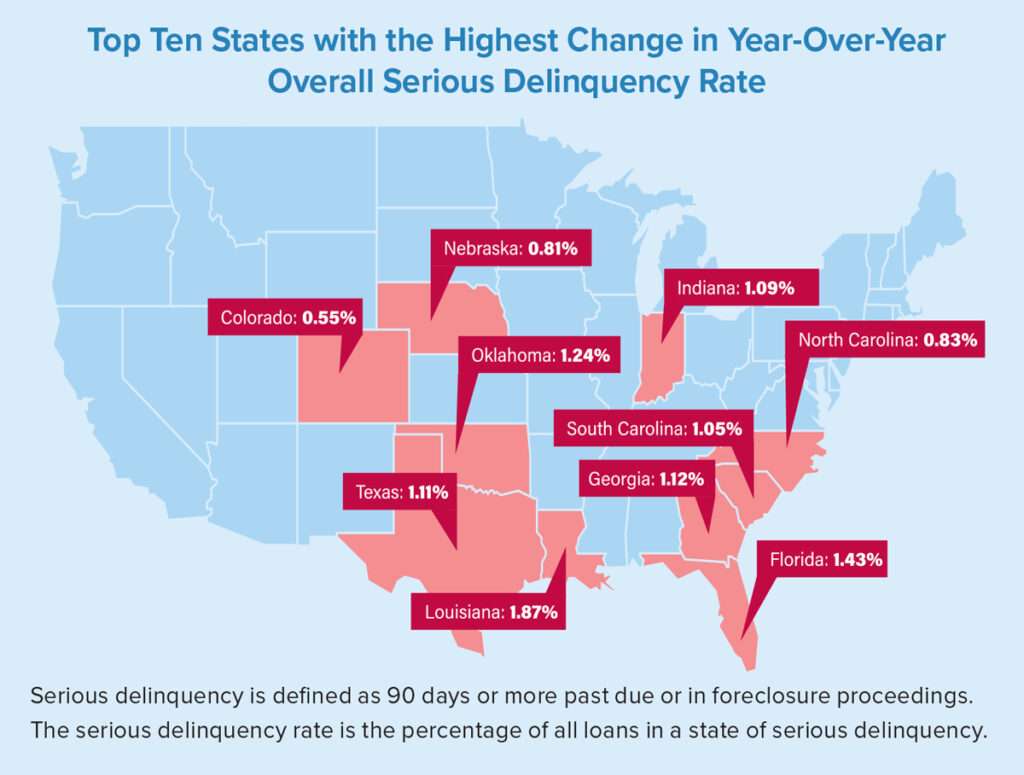

Mortgage delinquency rates vary significantly by region. Louisiana (1.87%) had the highest serious delinquency rate, followed by Mississippi (1.57%), New York (1.5%) and Florida (1.43%). In general, Southern and Eastern states experienced higher delinquency rates, while Western states saw lower rates.

While most U.S. states saw a slight uptick from last year, if you zoom in on certain states — Florida, South Carolina and Georgia, for instance — the picture changes. These states, which have seen significant upticks in delinquencies, have also faced considerable natural disasters, leading to higher insurance costs. While not always the case, states with the largest increases in escrow payments due to rising taxes and/or insurance costs often exhibited higher delinquency rates.

Take Florida as an example. Property taxes have jumped nearly 50% over the past five years. Insurance costs are also climbing fast, especially in areas at risk of hurricanes and floods. As a result, the average escrow payment, which typically covers taxes and insurance, rose 62% in the past five years. That’s on top of mortgage payments which include principal and interest charges that have increased for recent home buyers.

The last five years also have seen home prices, homeowners insurance and property taxes surge across the U.S. These rising costs reduce affordability for new buyers and squeeze existing homeowners’ budgets, often leading to payment difficulties and delinquencies.

The average monthly total mortgage payment in Florida in 2020 was $1,745, and while principal and interest have remained constant, an increase in the variable costs of taxes and insurance have resulted in a 7% increase in mortgage payments.

Even more shockingly, homebuyers who took the plunge in the last couple of years are paying an average total monthly mortgage of $2,617, which is 50% higher than for those who bought a home in 2020. As a result of stretching their budgets very thin and increasing homeownership cost variables, some of today’s homeowners are more vulnerable to falling behind on their mortgage payments.