For mortgage servicers selling properties at foreclosure auction, pricing below market and adjusting pricing quickly to adapt to changing market trends can help avoid the cost and risk of owning real estate. It also helps servicers achieve optimal price execution at auction, limiting loss severity while still producing maximum surplus funds for distressed homeowners.

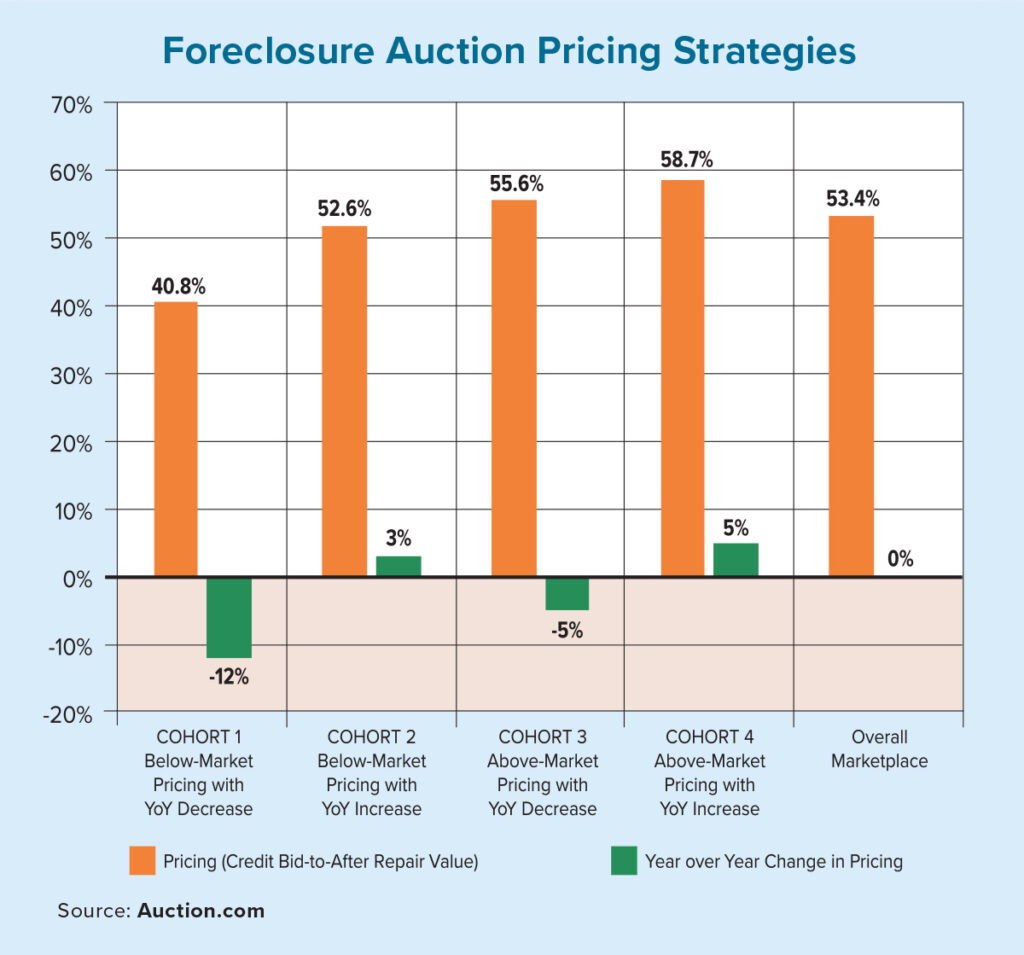

The data in the chart below are divided into four cohorts of sellers, each representing at least 15% of volume in the first half of 2025, and each with discrete pricing behavior. Foreclosure auction volume increased year over year for all four, consistent with the overall trend. The increase ranged from 2% for Cohort 3 to 17% for Cohort 2.

The pricing behavior is best examined by using two metrics: the average credit bid-to-after repair value ratio in the first half of 2025; and the change in that ratio compared to the first half of 2024. The credit bid at foreclosure auction is the minimum amount the seller is able or willing to take to sell the property, often called the “reserve price” in auction parlance.

Divergent sales rate performance

The divergent pricing strategies resulted in divergent auction outcomes, the most dramatic being the sales rate to third-party buyers at the foreclosure auction. The Cohort 1 strategy (price below market and quickly lower pricing to align with changing market conditions) clearly won for the sales rate outcome. It was an astounding 25 points above the next best sales rate among the cohorts and was the only one to post a year over year increase in sales rate.

By comparison, the pricing strategy employed by Cohort 4 (price above market and adjust pricing higher compared to a year ago) was the clear laggard, with the lowest sales rate and biggest year over year decrease in sales rate among the four.

Divergent proceeds performance

Despite the more proactive pricing strategy of Cohort 1, it still yielded proceeds above total debt owed at foreclosure auction on average. It was one of two cohorts to do so, along with Cohort 2. And although Cohort 2 produced a higher average winning bid-to-total debt ratio, remember that any winning bid surplus above total debt does not benefit loss severity for the foreclosing servicer or lender. It goes to the distressed homeowner after any junior liens are paid off.

Additionally, although the proceeds-to-after repair value ratio was three to four points lower for Cohort 1, that was likely a beneficial tradeoff in terms of loss severity for a sales rate advantage of 25-plus points. That substantial advantage means Cohort 1 sold much deeper into its portfolio at foreclosure auction than the others, reducing chances of realizing big losses on problem properties with extended holding times and bloated renovation costs.

Divergent surplus funds

On that note, the higher average winning bid-to-total debt ratio for Cohort 2 was on a much smaller share of properties brought to auction that sold to third-party buyers (the 25-point lower sales rate compared to Cohort 1). That meant that Cohort 1 still ended up producing potential surplus funds for 36.9% of all properties brought to foreclosure auction, just slightly higher than the 36.8% for Cohort 2. Cohort 4, with its above-market pricing that increased from a year ago, came in last for this metric with only 22.8% of properties brought to auction producing potential surplus funds.

Cohort 1 also outperformed all other cohorts in terms of the annual change in the average potential surplus produced at auction, up 2% from a year ago. All other cohorts saw a decrease in the average potential surplus produced at foreclosure auction.