Gold is surging — and not just in price. It’s rising in relevance, in symbolism and in strategic importance.

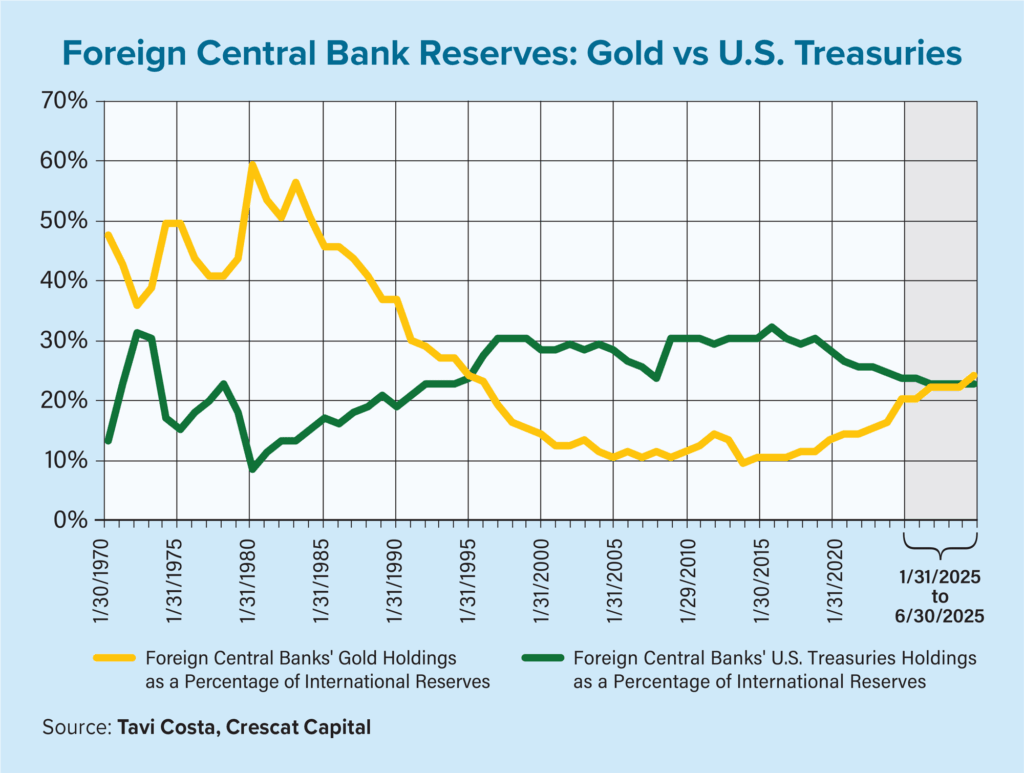

Foreign central banks have been leading the charge, and for the first time in nearly 30 years they hold more gold than U.S. Treasury bonds. It’s not just a diversification play, but a strategic pivot, reflecting a broader hedge against traditional reserve assets.

The stockpiling underway is not a short-term trade. It’s been happening for about six years, suggesting a deeper transformation in the global monetary system.

Further enforcing this trend was the decision by the U.S. and its allies to freeze more than $300 billion in Russian central bank reserves held in U.S. Treasurys in 2022. The move sent shockwaves through the international financial community, raising a fundamental question among U.S. allies and opponents: Are reserve assets held in U.S. institutions safe if they can be seized during periods of geopolitical crisis?

For many countries, the answer was, “No.” And the reaction has been swift.

China has dramatically increased its gold purchases while establishing gold-based trade settlement hubs. BRICS nations (Brazil, Russia, India, China and South Africa) are building alternatives to the SWIFT cooperative, a secure global bank messaging network overseen by the central banks of G10 countries, the European Central Bank and the National Bank of Belgium.

Alternatives are also being developed for the petrodollar framework (a global practice of exchanging oil for U.S. dollars instead of any other currency). Gold is emerging as a neutral, trusted asset as the world undergoes a multipolar financial transition.

Retail investors are taking notice, albeit more slowly. Historically, gold has been the domain of “gold bugs” — fringe voices warning of collapse and preaching the gospel of hard assets. That’s changing with financial media promoting the “debasement trade,” pairing gold with bitcoin as hedges against inflation and currency devaluation.

A presentation released by Citi Research shows spending on gold is at its highest level in more than 50 years — even more than what was seen during the 1980s oil shock. It sees this bull market for gold staying intact for the near future.

Major institutions are responding. Morgan Stanley Chief Investment Officer Michael Wilson recently spoke in favor of shifting base portfolio allocations for retail investors from the traditional 60/40 stock-bond split to a 60/20/20 model, breaking the bond portion to a 20/20 bond-gold split. Retail allocation to 20% gold would cause massive capital rotation out of bonds, given that gold is currently estimated to comprise less than 1% of retail investor portfolios.

The forces driving the price of gold higher are complex, though inflation plays a central role in the story. With the consumer price index, a common measure of inflation, rising at an annual rate of 3% in September, and long-term Treasury yields at 4.7% in early November, the real return on a 30-year bond is just 1.7%. That’s not a compelling return, especially when inflation risks remain elevated due to global trade tensions and potential monetary expansion, which could mean increasing money supply and lowering rates to stimulate economic activity.

Tariffs historically increase prices by passing on costs to consumers, reducing product availability and disrupting supply chains. They can trigger recessionary pressures, which can lead to money printing, additional inflation and heightened debasement concerns.

Gold’s rise also reflects the erosion of trust in government-issued “fiat currencies,” like the U.S. dollar or the euro, which are not backed by a precious metal or other asset. Gold is perceived as timeless, borderless and immune to political manipulation. Gold is not just a hedge — it’s a statement by investors and governments.

Financial institutions are beginning to grapple with this reality. With low real yields and high inflation risks, gold offers a compelling alternative. As more institutions pivot, price pressure builds. Advisers are now fielding tough questions from clients: “Why am I not in gold?”

That question is becoming harder to ignore. Some see it as a harbinger of crisis — financial, geopolitical or systemic. Short-term spikes in gold often coincide with market stress, liquidity squeezes or volatility surges. The recent spike in the Chicago Board Options Exchange’s CBOE Volatility Index (VIX) and widening secured overnight financing rate (SOFR) spreads suggest something is brewing beneath the surface.

It could all just be retail frenzy or speculation. Or it’s possible these real-time spikes in gold may be front-running a crisis we’ve yet to fully understand, whether war, debasement (leading to steep inflation and a decline in economic stability) or something else.

Gold could be signaling a transition from a dollar-dominated global system to a more diversified framework. Central banks are reallocating. Trade is being settled in rubles, yuan and gold. The petrodollar system is fading. Gold is at the center of a transformation not only about price action but potentially paradigm change.

If this trend continues, we may look back on this moment not as a speculative bubble, but as the beginning of a new monetary era.