Mortgage rates began 2025 around 7% and have declined to a range of 6.25% to 6.5% over the past several weeks. The rate movement has spurred mortgage activity, particularly among refinance applicants carrying plus-7% first mortgages of post-pandemic vintages.

In the background, however, easing mortgage rates have slowly eroded persistent mortgage rate lock-in effects disincentivizing financed homeowners from trading in ultra-low mortgage rates in the 3% to 5% range. Jilted lock-in effects can be observed in the rising share of outstanding mortgages with rates above 6%.

From the first quarter of 2023 to the first quarter of 2025, for example, the share of active mortgages with notes above 6% doubled from 9.5% to 18.9%, according to a new Redfin analysis of the Federal Housing Finance Agency’s National Mortgage Database, a nationally representative 5% sample of all first-lien, closed-end purchased or refinanced residential U.S. mortgages.

That climbed to 19.7% in the second quarter of 2025 — the highest share since 2015 and the last quarter for which complete data is available — a reflection of easing mortgage rate lock-in effects.

“More homeowners are deciding it’s worth moving even if it means giving up a lower mortgage rate,” said Chen Zhao, head of economics research at Redfin, in press release. “Life doesn’t stand still — people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

The share of outstanding mortgages with sub-3% mortgage rates dropped to 20.4% in the second quarter, down from a peak of 24.6% in the first quarter of 2021, Redfin reported. That means one-fifth of all mortgaged homeowners still have at least 300 basis points of breathing room between their existing mortgages and current market rates.

Mortgage giant Fannie Mae anticipates mortgage rates above 6% for the foreseeable future, potentially ending 2026 at 5.9%, coinciding with forecasted originations exceeding $2 trillion next year.

Redfin’s analysis complements a separate but related report from Realtor.com, suggesting that easing lock-in effects should disproportionately impact U.S. metros with elevated shares of mortgaged homeowners, such as Washington, D.C. (73.6%), Denver (72.9%) and Virginia Beach, Va. (70.7%).

“Meanwhile, metros with older populations and more outright owners, like Buffalo or Miami, may see a lower market-level response, even though lower rates are a difference-maker for some individuals in these markets,” said Danielle Hale, chief economist at Realtor.com, in the report.

Purchase demand has been slow to respond to recent dips in mortgage rates, though pending home sales for August as tracked by the National Association of Realtors showed 4% growth from July and 3.8% growth from August 2024.

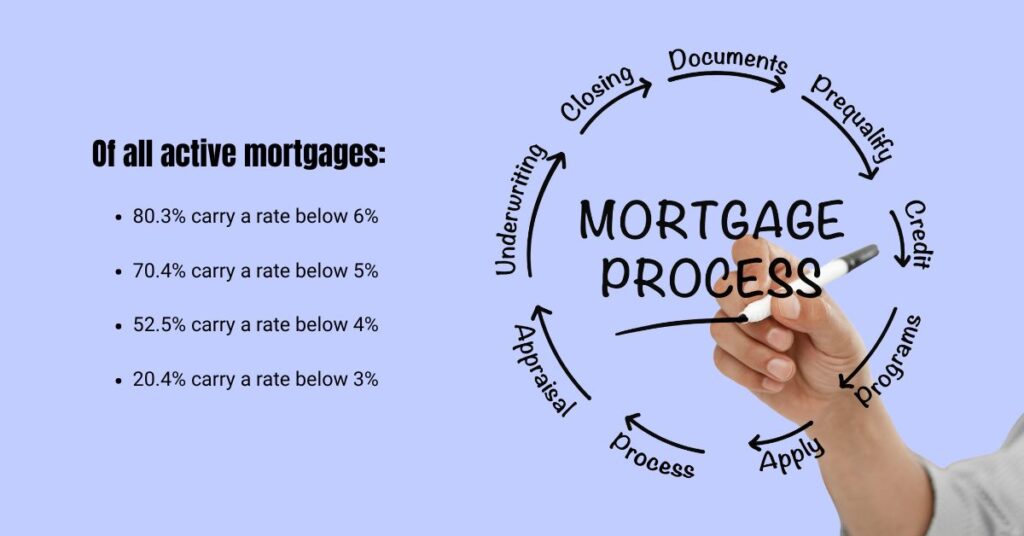

Today’s homeowners disperse along the following mortgage-rate spectrum:

- 80.3% carry a mortgage below 6%

- 70.4% carry a mortgage below 5%

- 52.5% carry a mortgage below 4%

- 20.4% carry a mortgage below 3%