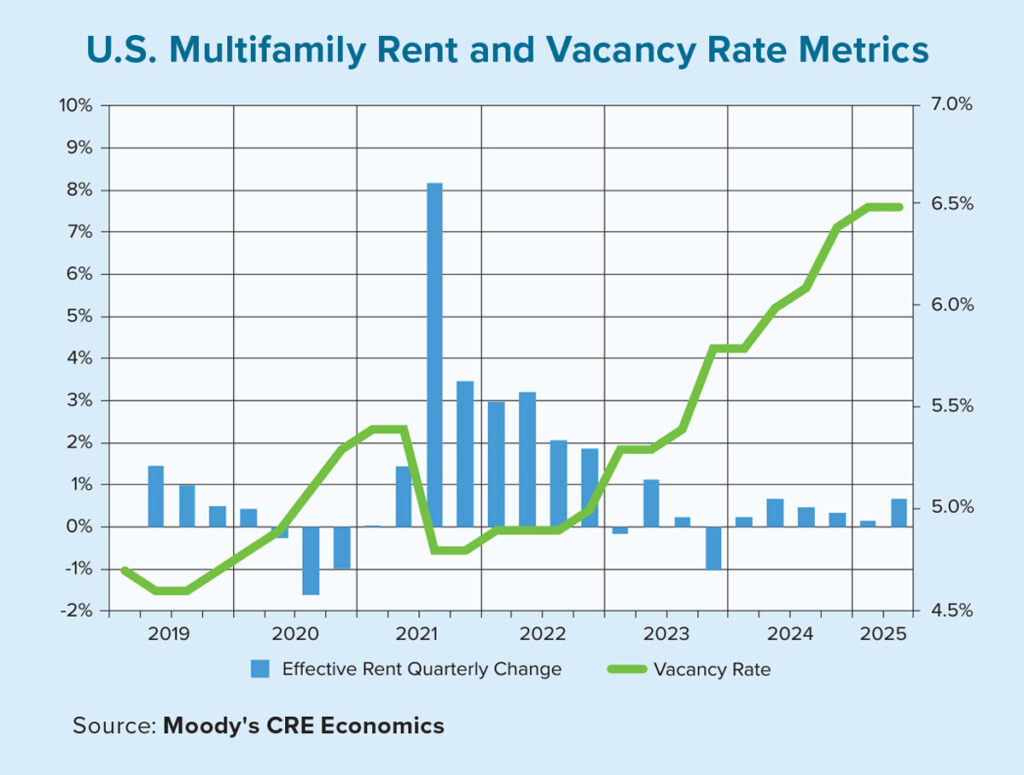

After more than two years of supply-side pressures, the rise in the nationwide multifamily vacancy rate effectively came to a halt in the second quarter of 2025. Although net absorption modestly outpaced total completions in June — a trend not seen since early 2023 — the vacancy rate was essentially unchanged sequentially at 6.5%.

Despite the improving conditions, the sector’s vacancy rate was still at its highest level since 2010, in part due to record levels of new construction over the past few years. For example, the U.S. multifamily market saw a significant increase in completions in 2023 and 2024, as delayed projects from the pandemic continued to materialize.

Also playing a role was the nation’s shifting migration patterns — especially driven by remote work — that helped fuel strong rental demand. Despite the influx of new supply, effective rent growth was positive for the sixth consecutive quarter, with Class B and C properties still maintaining tighter vacancy rates this economic cycle.

Regionally, the South Atlantic, Southwest and West reported significantly higher unit deliveries over the past two years compared with the Midwest and Northeast. The Texas cities of Austin and Dallas were notable as expanding metro areas, while Houston and Phoenix were among the top contributors to the new supply.

Even though rental demand has remained robust in many of these markets, the sheer volume of new supply outstripped net absorption, leading to rising vacancy rates. For context, across the 79 primary multifamily markets tracked by Moody’s Analytics, more than 3 in every 4 markets (or 61 of 79) in the second quarter of 2025 had higher vacancy rates than at the same time last year.

However, recent data suggest that peak deliveries have already occurred, contributing to the stabilization of the national vacancy rate at midyear. Similarly, the pace of new starts has slowed, as developers continue to face challenges.

Higher labor and construction costs, tighter lending conditions and higher interest rates all constrain project financing. This pullback in construction activity has helped to ease the oversupply pressures that have been driving vacancy rates higher. Consequently, Moody’s Analytics expects the sector’s vacancy rate to decline modestly to the low-6% area by the end of next year.

The abating supply is likely to be viewed positively for contributing to the stabilization of the sector’s vacancy rate. But there’s also a downside: The structural imbalance in the housing market is likely to be marginally prolonged. After years of underbuilding following the global financial crisis, the U.S. has a significant housing shortage.

While single-family homes represent the lion’s share of residential housing, a slowdown in multifamily deliveries nevertheless implies more time to close the housing gap. Furthermore, housing affordability remains a major challenge, especially in high-cost cities such as New York, which is experiencing elevated rent-to-income ratios. The problem is so acute, the issue has taken center stage in the city’s mayoral race in November.

The multifamily sector is settling into a new period of stabilization. While the nationwide multifamily vacancy rate was at its highest level in approximately 15 years, in aggregate, new supply is being successfully digested by the market.

As supply pressures continue to ease, rental demand has remained relatively resilient. Vacancy rates should gradually decline and rent growth will likely pick up in earnest. It may be a bumpy road ahead, but for now, the sector appears to be finding its footing.