The slew of post-rate cut speaking engagements by Federal Reserve officials continued Tuesday, with high-profile speeches by Chairman Jerome Powell and Fed Governor Michelle Bowman presenting differing takes on upside risks to inflation and downside risks to the labor market.

Their comments followed Stephen Miran’s first speech as a Fed governor on Monday. The newly installed central banker downplayed tariff-driven inflation and called for the benchmark federal funds rate to be a full two percentage points lower than its current range of 4% to 4.25%.

Meanwhile, Raphael Bostic and Beth Hammack, the respective heads of the Fed’s Atlanta and Cleveland banks, signaled a more cautious approach to interest rate cuts, warning of rising inflation as companies that have been eating tariff-related costs begin to pass those expenses on to consumers.

Powell, in prepared remarks at an economic conference in Rhode Island, echoed Bostic’s and Hammack’s comments about the delayed impacts of tariffs, saying “uncertainty around the path of inflation remains high.”

“Tariff increases will likely take some time to work their way through supply chains,” Powell stated. “As a result, this one-time increase in the price level will likely be spread over several quarters and show up as somewhat higher inflation during that period.”

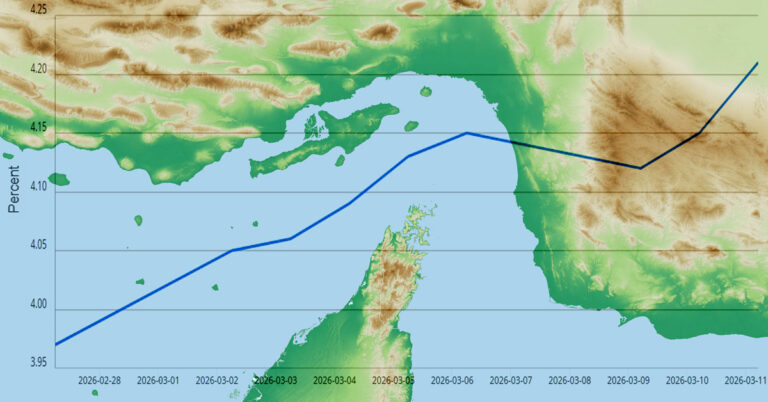

On Friday, the Bureau of Economic Analysis is set to release its updated personal consumption expenditures (PCE) price index for August, which is the Fed’s preferred measure of inflation. Powell said the latest available data indicate PCE prices likely rose 2.7% on a 12-month basis last month, which would be the furthest that index has been from the Fed’s 2% inflation target this year.

But Powell also repeated the headline statement from his Sept. 17 press conference following the Fed’s quarter-point rate cut announcement, saying “there is no risk-free path” as the central bank walks the thin line of addressing its dual mandate of promoting both stable consumer prices and maximum employment.

On the employment side, Powell noted “there has been a marked slowdown in both the supply of and the demand for workers — an unusual and challenging development.” He added that the recent pace of job creation appears to be running below the “breakeven” mark to hold the unemployment rate steady, but that the ratio of unemployed persons per job opening remains broadly stable at 1.0.

Bowman pushes for proactive thinking

The Fed rate cut in September represented a victory lap of sorts for Bowman, who had dissented and pushed for a quarter-point cut at the previous Federal Open Market Committee meeting in July, when the FOMC held rates steady.

In a speech Tuesday at a Kentucky Bankers Association convention, Bowman warned that “the labor market has become more fragile and could deteriorate more significantly in the coming months,” while also expressing her belief that “tariffs will have only a small and short-lived effect on inflation going forward.”

Bowman explicitly pushed for additional rate cuts, stating: “Assuming the economy evolves as I expect, last week’s action should be the first step to bring the federal funds rate back to its neutral level.”

Looking forward, Bowman advocated for a proactive approach to monetary policy that is less reliant on the interpretation of the most recent data points.

“A strict interpretation of data dependence is inherently backward-looking and would guarantee that we remain behind the curve, requiring us to overcorrect in the future,” Bowman said. “I think we should consider reframing our focus from overweighing the latest data to a proactive forward-looking approach and a forecast that reflects how the economy is likely to evolve going forward.”