The Residential Transition Loan (RTL) market provides short-term capital for real estate investors involved in time-sensitive fix-and-flip or bridge financing projects. Typically spanning nine to 24 months, RTLs command high fixed rates, reflecting higher credit risk, project uncertainty and streamlined underwriting.

Lenders often fund these loans using a combination of equity (usually 20-30%) and floating-rate, Secured Overnight Financing Rate (SOFR)-indexed warehouse lines. Due to large capital cushions, high net interest margins (NIM) and the relatively short tenor of the loans, many originators and investors forgo proactive interest rate risk management. They accept the mismatched risk between their fixed-rate loans and their floating-rate financing facilities.

Recent market history has shown interest rates can shift unpredictably, even within a single year. Such volatility poses significant threats to lenders’ net interest margins, potentially impairing values of loan pools and eroding overall profitability. In response to the growing appetite for RTL securitizations, lenders are selling loan pools to aggregators or arranging securitizations themselves.

This process often involves leverage and financing, which is where interest rate hedging becomes not just prudent, but critical. Liquid and easily accessible exchange-traded SOFR interest rate swap futures make managing this risk simple, efficient and accessible to all RTL lenders.

Why hedging?

Hedging the floating-rate liabilities that support RTL lending helps lenders eliminate mismatch risk by aligning the short-term, SOFR-indexed funding with the longer-term, fixed-rate nature of the loan assets. It ensures consistency in profitability by securing the spread between lending rates and borrowing costs. Fixed borrowing costs provide greater predictability, allowing lenders to operate with more aggressive capital structures.

For example, a lender can use exchange-traded interest rate swap futures to convert floating-rate warehouse debt to a fixed rate. This synchronizes the tenor and rate of loan funding with the fixed-rate loans a lender originates. This removes the uncertainty from its funding liability and empowers the lender to confidently pursue a more aggressive capital structure — potentially reducing equity requirements to 10-15% and backfilling that capital with more floating-rate, SOFR-indexed funding.

Yield curve opportunities

Beyond reducing risk, interest rate hedging helps lenders capitalize on favorable market dynamics. In an inverted yield curve environment, as of September 8, 2025, the 1-year SOFR rate at 3.6% was trading more than 0.8% below the overnight SOFR rate of 4.42%. Market expectations of future Federal Reserve rate cuts drove this inversion. The interest rate markets, through the pricing of interest rate futures, were forecasting six 0.25% basis point cuts over the next year.

By trading exchange-traded swap futures, market pricing presented lenders with the opportunity to lock in a fixed rate for one year that was more than 0.8% lower than the overnight SOFR financing rate. This would have realized an immediate spread increase of 0.8% over the already attractive spread between their fixed-rate loans and their short-term, SOFR-based financing. This tactical use of hedging removes the risk of future rate changes while providing an immediate boost to profitability.

Building a predictable model

In the increasingly competitive RTL lending sector, stability is as vital as growth. Matching the tenor of a lender’s debt with the average maturity of their loan portfolio not only reduces earnings volatility but also makes financial forecasting far more reliable.

In practice, this leads to a more consistent Return on Equity (ROE), even when the broader interest rate environment shifts. Lenders will also find that having an adequately framed interest rate risk management strategy can improve their financing costs from warehouse lenders, who often give borrowers credit for understanding and mitigating the tail risks that can lead to wider lending spreads.

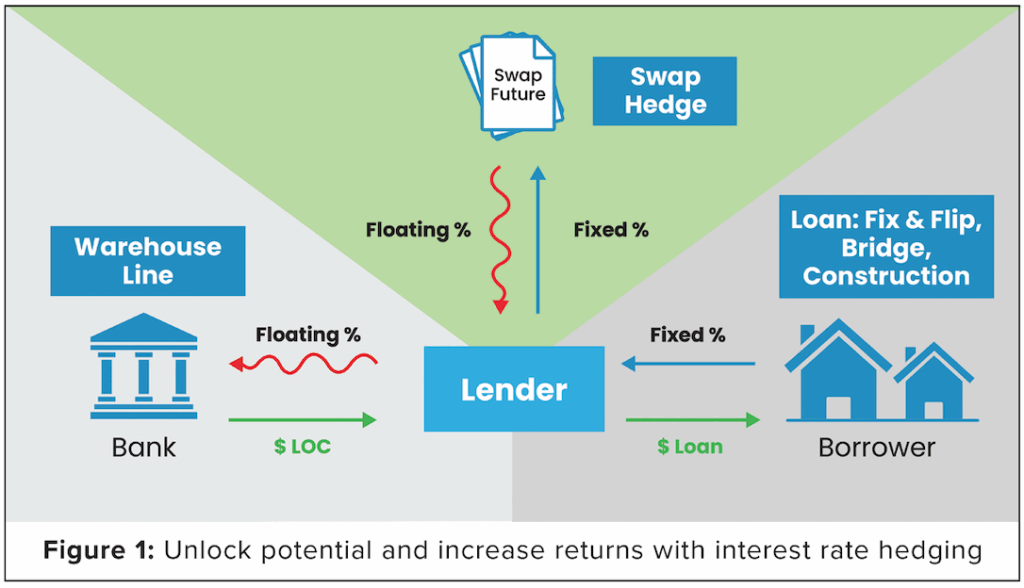

As illustrated in Figure 1, exchange-traded interest rate swap futures offer a simple, easily accessible and standardized way to hedge across a variety of tenors. In the illustration, a lender uses swap futures to offset the mismatch of interest risk between the loans it is purchasing and the warehouse lines being drawn from its bank. The resulting effect is a fixed interest margin between the loans purchased and the hedged, fixed financing. These futures are exchange-traded, eliminating counterparty risk through central clearing, and operational complexities are reduced compared to traditional over-the-counter (OTC) swaps.

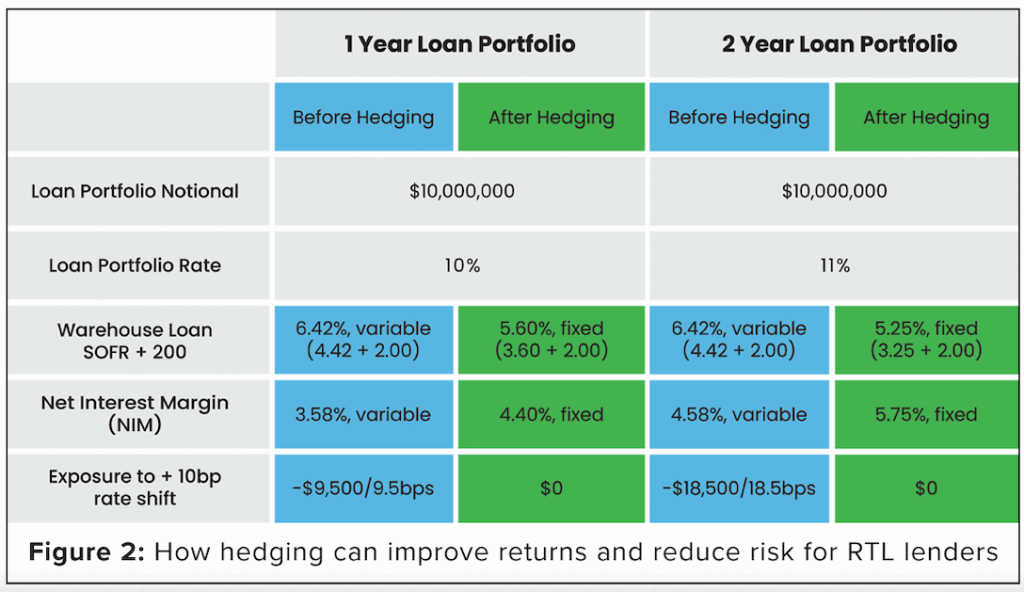

For private lenders, mortgage companies and lending institutions active in the RTL space, hedging interest rate exposure is no longer just a defensive measure — it’s a performance-enhancing tool (Figure 2). Given that interest rate volatility is likely to persist, lenders who proactively manage their funding risk tend to improve client pricing, increase profitability and reduce earnings volatility associated with swings in interest rates. Prudent hedging programs help lenders gain a strategic and competitive edge.

By leveraging interest rate swap futures, RTL lenders can transition from a reactive model of margin protection to a proactive strategy of portfolio optimization. The result is a more stable, scalable and resilient lending model built to thrive across various economic cycles.