A global economy marked by declining consumer spending, high unemployment rates and sluggish manufacturing output would normally cause great concern for industrial real estate property owners and investors. Although flex properties and those used for research and development (R&D) are exhibiting some of this weakness, the warehouse subsector is poised to weather the short-term storm and be a potential long-term bright spot in an otherwise cloudy sky.

Prior to the COVID-19 pandemic, the industrial sector was weakening as it headed toward the latter stages of its cycle. Speculative development increased supply at a time when the global economy softened. Gross domestic product growth struggled to break an annualized rate of 2% during any quarter in 2019.

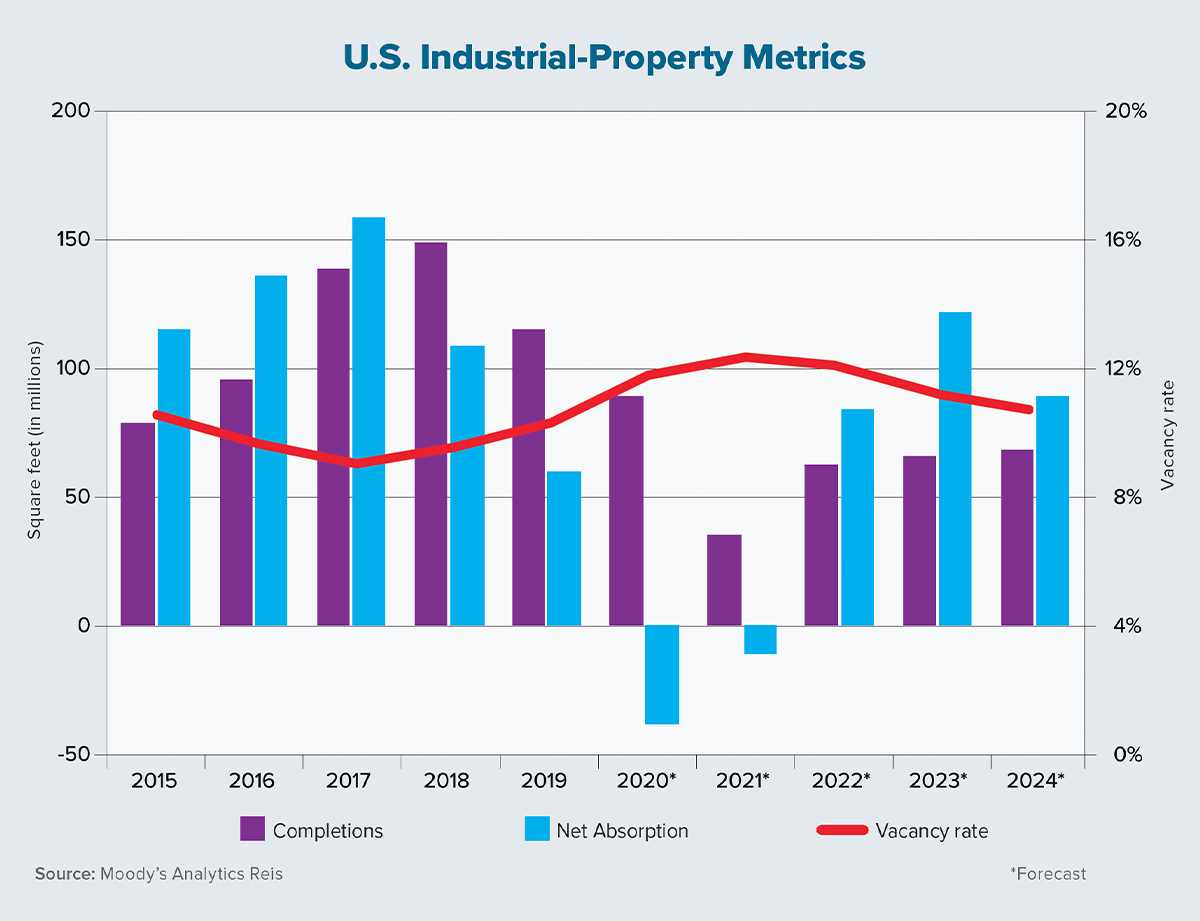

Tensions with China and general uncertainty regarding global trade led many real estate and capital-market participants to pause their industrial-property activity. At year-end 2019, flex and R&D space had a vacancy rate slightly below 10% while the warehouse subsector ended the year with a 10.1% vacancy rate, up from its expansion-period low point of 9% in late 2017, according to Moody’s Analytics Reis data. Rent growth for these subsectors also had slowed in recent quarters, with each averaging a quarterly increase of about 0.5% over the past two years.

Data from the first six months of 2020 clearly illustrate the beginnings of commercial real estate market stress due to the pandemic. From an ordinal perspective, industrial properties are easily the least affected of the major asset classes, and forecasts remain mostly positive in both the short and long run.

E-commerce has blossomed and the share of online spending across all U.S. retail sales could increase from about 10% last year to nearly 25% in 2020. This shift in shopping habits will cause a sizable increase in warehousing needs.

In June 2020, Prologis chief financial officer Tom Olinger stated that “e-commerce requires roughly three to three-and-a-half times the warehouse space than a traditional brick-and-mortar retailer would need.” Online companies must hold more stock and variety to be competitive, and also need more space for packaging.

Other potential sources of industrial real estate growth include increases of strategic reserves, liquidation events and an ever-growing need for data storage. All levels of government will take a hard look at how they prepare for future pandemics. Increased strategic reserves of medical supplies and household necessities may be a result. Additionally, some retailers — such as grocery and home-improvement stores — may decide to bulk up their inventories. The pandemic has exposed weaknesses in their supply lines.

There continue to be possible risks for the industrial real estate sector and they are growing more probable as COVID-19 has already persisted in the U.S. longer than many anticipated. A double-dip or protracted recession will slow consumer spending to a point where industrial will suffer along with other sectors.

Reshoring or increasing trade with Mexico is a real possibility and would increase industrial space in cities such as Houston. Finally, industrial location patterns are expected to change as smaller warehouses spread more evenly throughout the country and become the norm. This evolution will support last-mile delivery and the ability to reach nearly all consumers within a day.

Interestingly, this could be a surprising boon to retail-property owners with vacant space near population centers. Converting these properties to distribution space is a cost-effective possibility. The sky may not be completely clear, but from both a short- and long-term perspective, industrial is a likely bright spot for commercial real estate owners and investors. ●