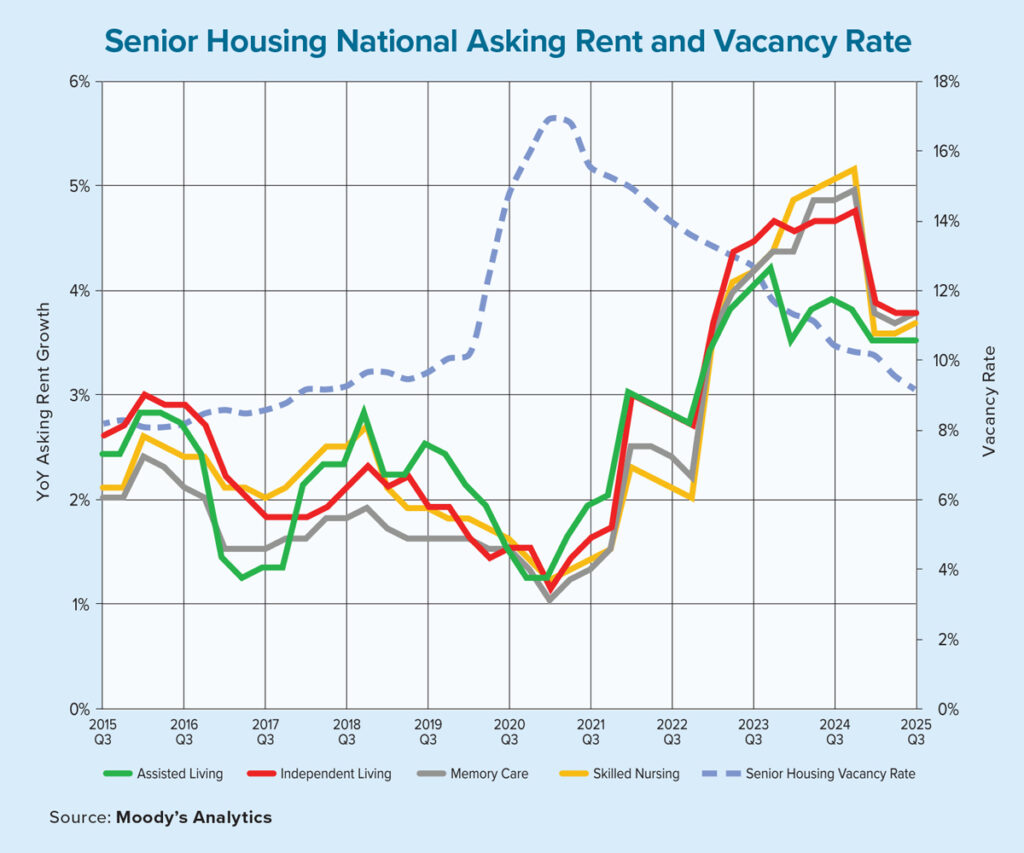

The senior housing sector has experienced a strong recovery from its pandemic challenges and has now returned to pre-pandemic levels. Vacancy rates have steadily decreased for 18 consecutive quarters, reaching 9.1% in the third quarter of 2025, the lowest level since 2018. This trend is primarily driven by increasing demand from America’s aging population, particularly baby boomers, alongside limited growth in inventory due to high interest rates and financing difficulties.

Annual inventory growth remains minimal at just 0.3%, benefiting existing operators as new construction struggles to keep up with demand. Over the last two years, rents in senior housing have risen faster than those in multifamily housing and the consumer price index (CPI), reflecting stronger demand and pressure from rising labor costs. Additionally, robust job growth in the health care sector highlights the demographic undercurrents driving the senior housing market as the baby boomer generation ages.

Vacancy rates across four senior housing care types — including independent living, assisted living, memory care and skilled nursing — have consistently declined, with memory care experiencing the largest drop of 80 basis points in the third quarter of 2025. Rent growth remains robust, ranging from 3.6% to 3.8% year over year across subsectors, though signs of a slowdown in rent growth are emerging due to affordability challenges.

Current average rents vary significantly, from an average of $3,940 in independent living to $10,706 in skilled nursing, reflecting the significance of labor costs in the sector. Despite recent improvements, five-year rent growth in senior housing is between 17.6% to 18.7% based on care type, trailing CPI growth for urban consumers of 24.8% and multifamily rent increases of 27.9%, as recent rent growth still hasn’t compensated for senior housing’s sluggish pandemic-era performance.

However, as the sector plays catch-up, limited construction activity driven by high interest rates and economic uncertainty has constrained inventory growth, with only 4,853 new units added year over year. That represents only a 0.3% annual growth rate, underscoring a steady decline in completions over the last five years. The sector’s annual growth rate averaged 1.8% in the five years prior to the pandemic.

In the third quarter of 2025, 86% of tracked markets showed declining vacancy rates, with all five geographic regions experiencing reductions ranging from 20 to 50 basis points. The Southwest region, which includes Texas and Arizona, saw a 50-basis-point decline in the third quarter but still has the highest vacancy rate at 11.2%. The Northeast, Southeast and West regions now have single-digit vacancy rates, and the Midwest is expected to join them in the fourth quarter, having dropped 40 basis points to a 10.1% vacancy rate in the third quarter.

The senior housing sector is expected to continue growing due to increasing demand from aging baby boomers, though key questions now center on when construction will pick up. Vacancy rates are anticipated to decline further, given the lack of new supply and steadily rising demand, while rent growth is expected to stabilize despite challenges related to affordability.

Although new construction will likely increase as interest rates decrease, macroeconomic uncertainties may delay these developments. Existing operators are likely to benefit from strong demand and steady rent growth, while developers may face challenges related to financing and the timing of new projects. Overall, the long-term outlook for the sector remains positive, supported by demographic trends, with uncertainty related to renter affordability and the labor market shaping its path forward.