Surging homeowners insurance premiums have posed a persistent threat to housing affordability over the past year, with costs rising faster than incomes in several states, hitting lower-income households the hardest.

That’s according to a new study from the Federal Reserve Bank of Chicago, which oversees the 7th Federal Reserve District spanning all of Iowa and most of Michigan, Illinois, Indiana and Wisconsin.

“The rise in homeowners insurance costs may lead to no-win choices for long-time homeowners who can neither afford their premiums nor the cost of repair if they lower their premiums by increasing their deductible (or, for those without a mortgage, forgo insurance altogether),” the report noted.

Continuation in the trend may cause new homebuyers to be “priced out of certain markets because of high homeowners insurance premiums,” the reports’ authors added. As premiums have skyrocketed in recent years, the mortgage industry has faced associated hurdles in qualifying borrowers for affordable home loans.

As of 2021, more than 35 million people lived across the 7th District, which includes the major Midwest hubs of Chicago, Detroit, Milwaukee, Indianapolis and Grand Rapids, Mich. According to 2023 data from the U.S. Bureau of Economic Analysis, median income across the broader Midwest region was $76,800 in 2023, lagging the U.S. median of $82,600, according to Chicago Fed data.

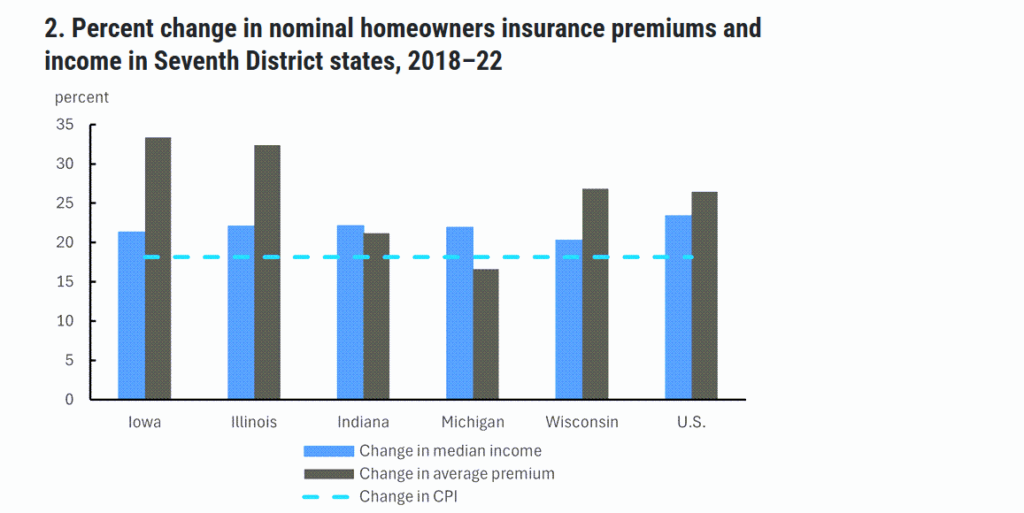

Higher rebuilding costs from elevated labor and material expenses, more intense and frequent storm damage to properties, and a rise in reinsurance costs drove a 25% average increase in home insurance premiums nationwide between 2018 and 2022, the Chicago Fed said. Households across the 7th District typically spend less of their income on homeowners insurance than the national average, but conditions vary widely state to state.

Without adjusting for inflation, Chicago Fed researchers found that in three of the five states in the district, homeowners insurance premium increases exceeded the national average growth rate. Premiums rose 33% in Iowa over that four-year span, 32% in Illinois and 27% in Wisconsin, while only increasing 17% and 21% in Michigan and Indiana.

Analyzing American Community Survey data from the U.S. Census Bureau, the analysis also found that premium growth outpaced median income growth on a percentage basis in Iowa, Illinois and Wisconsin from 2018 to 2022, though not in Michigan and Indiana.

The Chicago Fed compared average premium to median income in 2022 to assess “the extent to which households’ budgets are impacted by insurance prices.” Households in Michigan’s lowest-income zip codes spent 3.2% of their annual income on homeowners insurance — compared to 1.7% for middle-income earners, 1.2% for the top earners in the state, and above the national rate of 2.8% for the lowest income bracket.

While the lowest-income earners paid the highest share of their annual earnings on homeowners insurance in all 7th District states, Wisconsin emerged as the most affordable in 2022. Only 2% of annual income for the lowest earners went to premiums that year, compared to 1.4% for middle-income residents and 1.1% for top-income earners.

Changes in that premium-to-earnings ratio also fluctuated across states in the 7th District, with variations “primarily driven by differences in premium increases rather than differences in income growth,” said the Chicago Fed. Nationally, the lowest-income earners paid 5% less annual income on home insurance premiums in 2022 than 2018, as that earnings bracket saw incomes rise 28% compared to 22% premium growth.

While Michigan had the highest ratio of average homeowners insurance premium to median income among lowest-income earners, it also posted the largest improvements in that ratio across all income brackets due to slower premium growth from 2018 to 2022. Accelerated premium hikes in Iowa and Illinois caused insurance to grow less affordable.

For middle-income earners, the premium-to-earnings ratio increased — reflecting worse affordability — by 13% in Illinois and 11% in Iowa, compared to 6% growth in Wisconsin and a national rate of 2%. The ratio did not change for middle-income households in Indiana, while the ratio declined by 2% in Michigan. The ratio declined across all income brackets in Michigan, the only state in the 7th District to do so.

Nationwide, homeowners insurance cancellations for nonpayment were highest in zip codes with the lowest median household incomes, a reflection of higher-income households’ broader capacity to absorb the payment shock of premium increases.

Rates of around 2% for nonpayment cancellations in 7th District states exceeded the national rate of around 1.6% from 2018 to 2022. However, nonpayment cancellation rates trended down in the district from 2.3% in 2018 and 2019 to 1.9% in 2022, “while this rate ticked up slightly in the entire U.S. over this span,” the Chicago Fed reported.